Question: Please answer those question with round first two decimals Suppose you have the following possible risky investments (A,B,C,D) and a risk free investment (RF) where

Please answer those question with round first two decimals

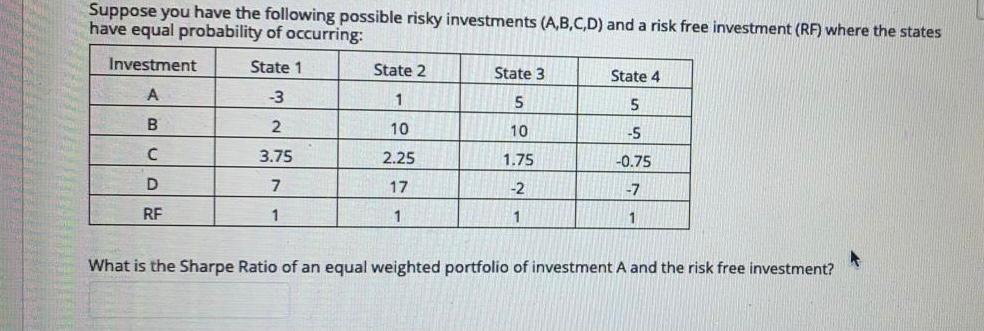

Suppose you have the following possible risky investments (A,B,C,D) and a risk free investment (RF) where the states have equal probability of occurring: Investment State 1 State 2 State 3 State 4 -3 1 5 5 B 2. 10 10 -5 3.75 2.25 1.75 -0.75 D 7 17 -2 - 7 RF 1 1 1 1 What is the Sharpe Ratio of an equal weighted portfolio of investment A and the risk free investment

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock