Question: Please answers c,d, & e 2. A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a

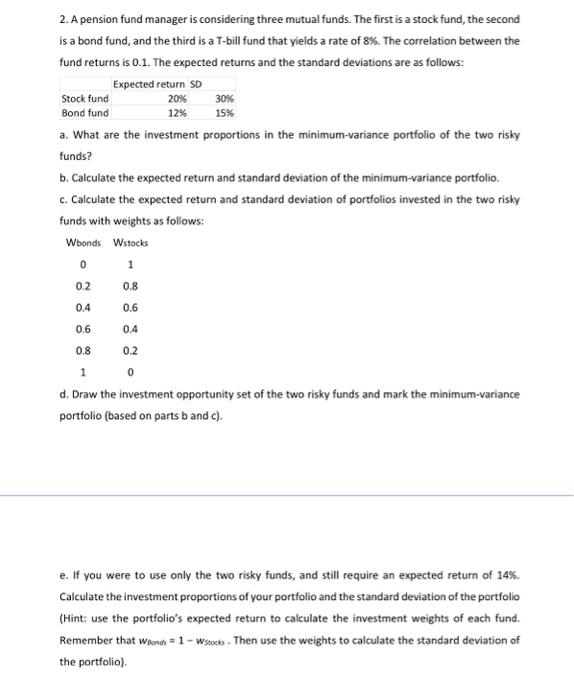

2. A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a bond fund, and the third is a T-bill fund that yields a rate of 8%. The correlation between the fund returns is 0.1 . The expected returns and the standard deviations are as follows: a. What are the investment proportions in the minimum-variance portfolio of the two risky funds? b. Calculate the expected return and standard deviation of the minimum-variance portfolio. c. Calculate the expected return and standard deviation of portfolios invested in the two risky funds with weights as follows: d. Draw the investment opportunity set of the two risky funds and mark the minimum-variance portfolio (based on parts b and c). e. If you were to use only the two risky funds, and still require an expected return of 14%. Calculate the investment proportions of your portfolio and the standard deviation of the portfolio (Hint: use the portfolio's expected return to calculate the investment weights of each fund. Remember that wbond=1wstowb. Then use the weights to calculate the standard deviation of the portfolio)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts