Question: please attach the excel file Compute for the portfolio risk using the following given: weight AUB weight Bank of Commerce correlation coefficient Union Bank 12/24/2021

please attach the excel file

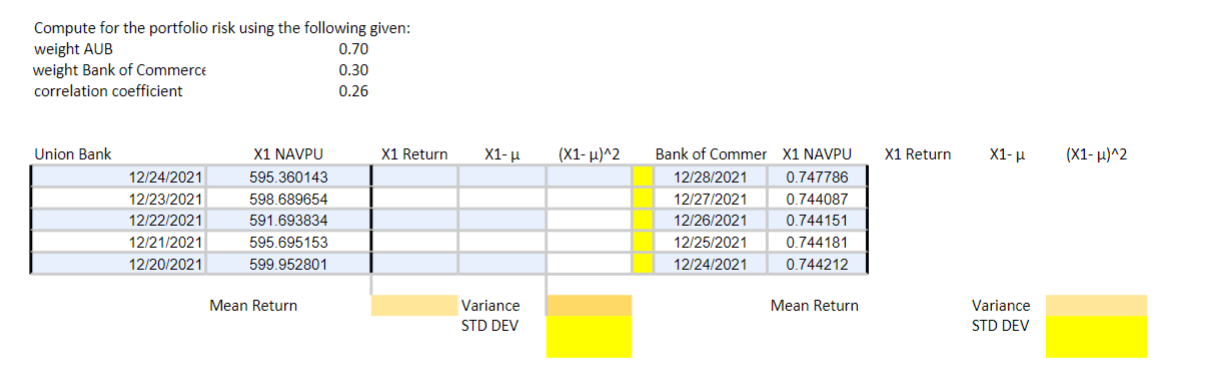

Compute for the portfolio risk using the following given: weight AUB weight Bank of Commerce correlation coefficient Union Bank 12/24/2021 12/23/2021 12/22/2021 12/21/2021 12/20/2021 X1 NAVPU 595.360143 598.689654 591.693834 595.695153 599.952801 Mean Return 0.70 0.30 0.26 X1 Return X1- Variance STD DEV (X1-)^2 Bank of Commer 12/28/2021 12/27/2021 12/26/2021 12/25/2021 12/24/2021 X1 NAVPU 0.747786 0.744087 0.744151 0.744181 0.744212 Mean Return X1 Return X1- Variance STD DEV (X1-)^2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock