Question: PLEASE BE QUICK AS YOU CAN Suppose my utility function for asset position x is given by u(x)=In x. I now have $20000 and am

PLEASE BE QUICK AS YOU CAN

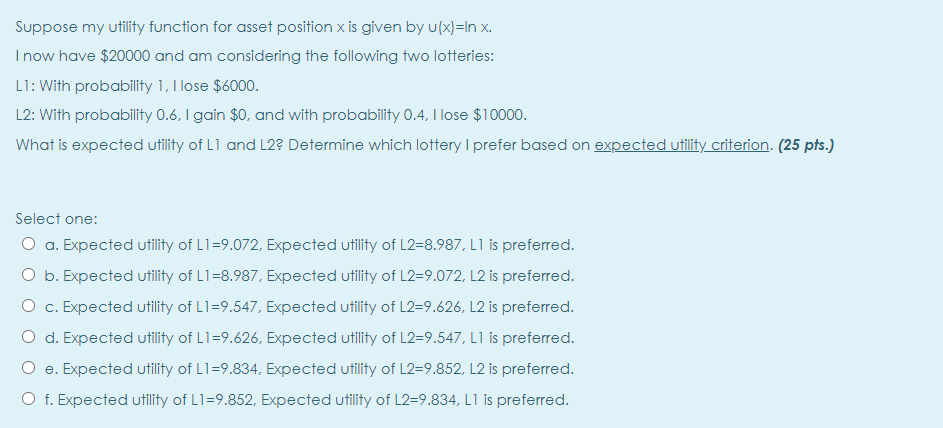

Suppose my utility function for asset position x is given by u(x)=In x. I now have $20000 and am considering the following two lotteries: L1: With probability 1, I lose $6000. L2: With probability 0.6, I gain $0, and with probability 0.4, I lose $10000. What is expected utility of L1 and L2? Determine which lottery I prefer based on expected utility criterion. (25 pts.) Select one: O a. Expected utility of L1=9.072, Expected utility of L2=8.987, L1 is preferred. O b. Expected utility of L1=8.987, Expected utility of L2=9.072, L2 is preferred. O c. Expected utility of L1=9.547, Expected utility of L2=9.626, L2 is preferred. O d. Expected utility of L1=9.626, Expected utility of L2=9.547, L1 is preferred. e. Expected utility of L1=9.834, Expected utility of L2=9.852, L2 is preferred. f. Expected utility of L1=9.852. Expected utility of L2=9.834, L1 is preferredStep by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock