Question: Please be specific, answer all parts step by step, and show the formula you use. Thank you! You have been provided the following data on

Please be specific, answer all parts step by step, and show the formula you use. Thank you!

Please be specific, answer all parts step by step, and show the formula you use. Thank you!

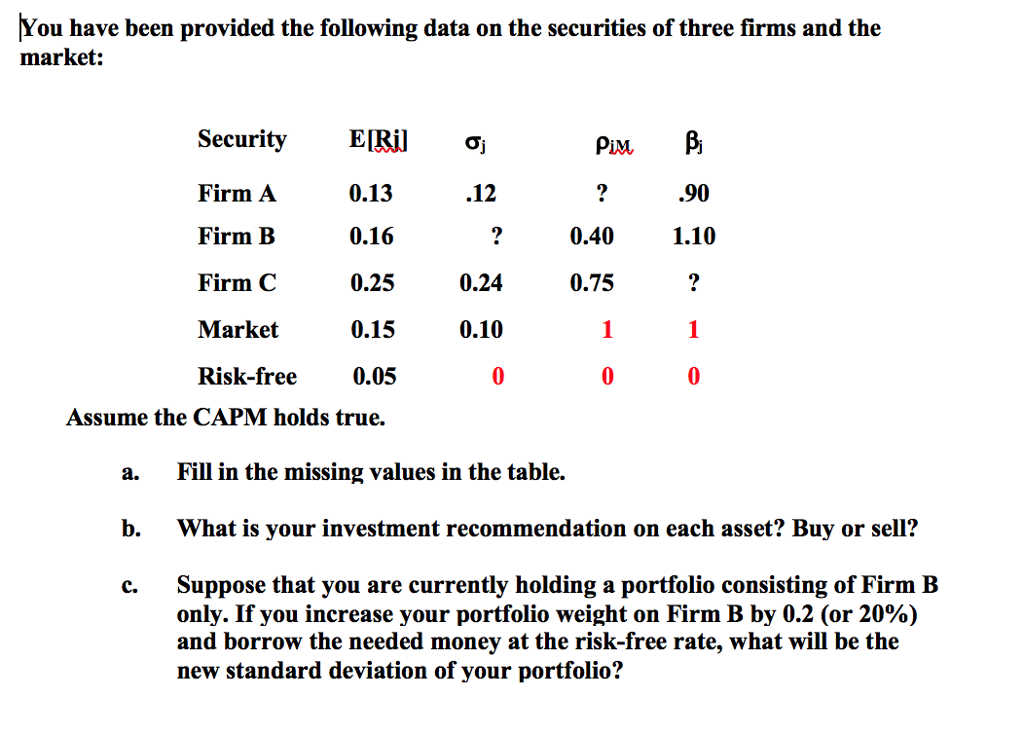

You have been provided the following data on the securities of three firms and the market: Security Firm A Firm B Firm C Market Risk-free ElKil 0.13 0.16 0.25 0.15 0.05 .90 1.10 j .12 0.40 0.24 0.75 0.10 Assume the CAPM holds true. a. Fill in the missing values in the table. b. What is your investment recommendation on each asset? Buy or sell'? c. Suppose that you are currently holding a portfolio consisting of Firm EB only. If you increase your portfolio weight on Firm B by 0.2 (or 20%) and borrow the needed money at the risk-free rate, what will be the new standard deviation of your portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts