Question: please do 2.4 -( 0 2.3 Assume that we have three assets with a covariance matrix of returns 0.01 0.01 0 C = 0.01 0.02

please do 2.4

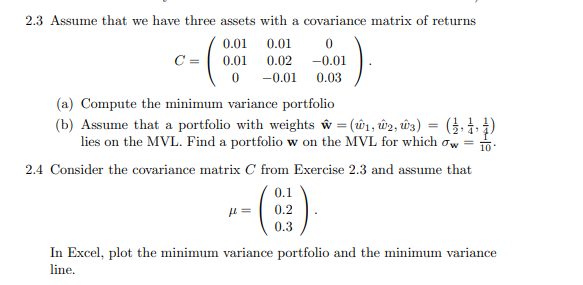

-( 0 2.3 Assume that we have three assets with a covariance matrix of returns 0.01 0.01 0 C = 0.01 0.02 -0.01 -0.01 0.03 (a) Compute the minimum variance portfolio (b) Assume that a portfolio with weights W =(W1, W2, W3) = (1, 3, 5) lies on the MVL. Find a portfolio w on the MVL for which ow = 2.4 Consider the covariance matrix C from Exercise 2.3 and assume that 0.1 0.2 0.3 In Excel, plot the minimum variance portfolio and the minimum variance line. H -() -( 0 2.3 Assume that we have three assets with a covariance matrix of returns 0.01 0.01 0 C = 0.01 0.02 -0.01 -0.01 0.03 (a) Compute the minimum variance portfolio (b) Assume that a portfolio with weights W =(W1, W2, W3) = (1, 3, 5) lies on the MVL. Find a portfolio w on the MVL for which ow = 2.4 Consider the covariance matrix C from Exercise 2.3 and assume that 0.1 0.2 0.3 In Excel, plot the minimum variance portfolio and the minimum variance line. H -()

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts