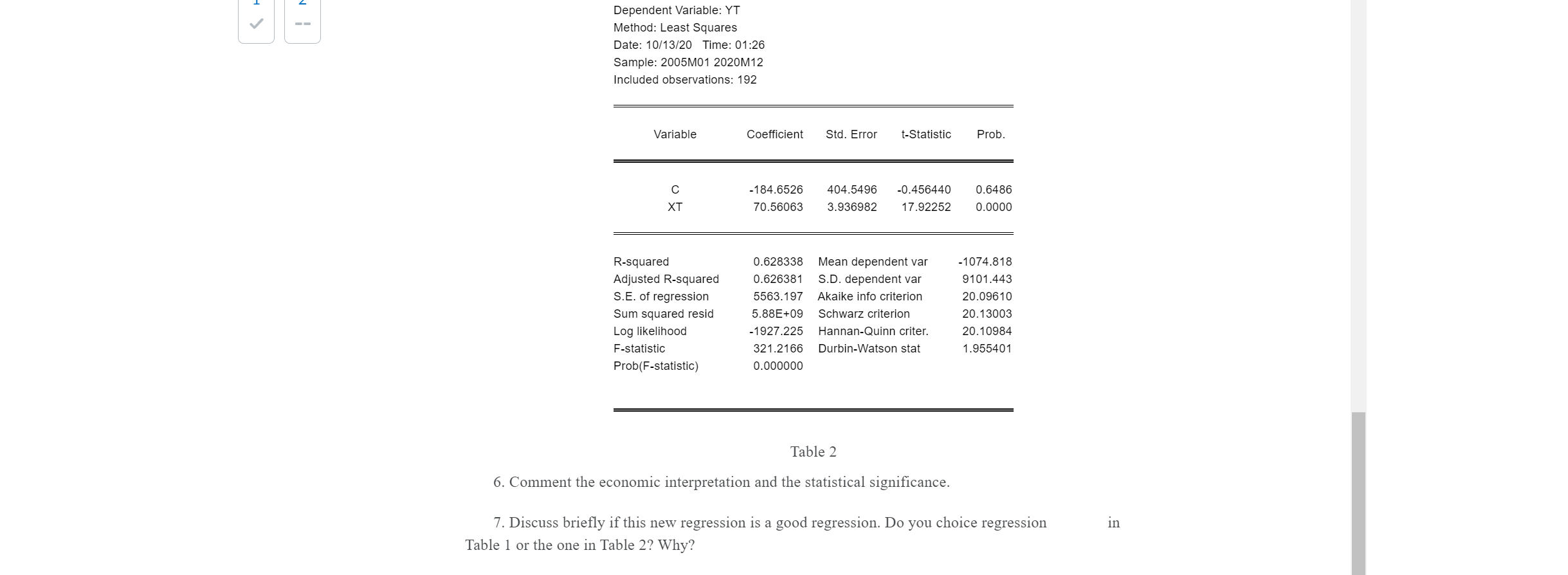

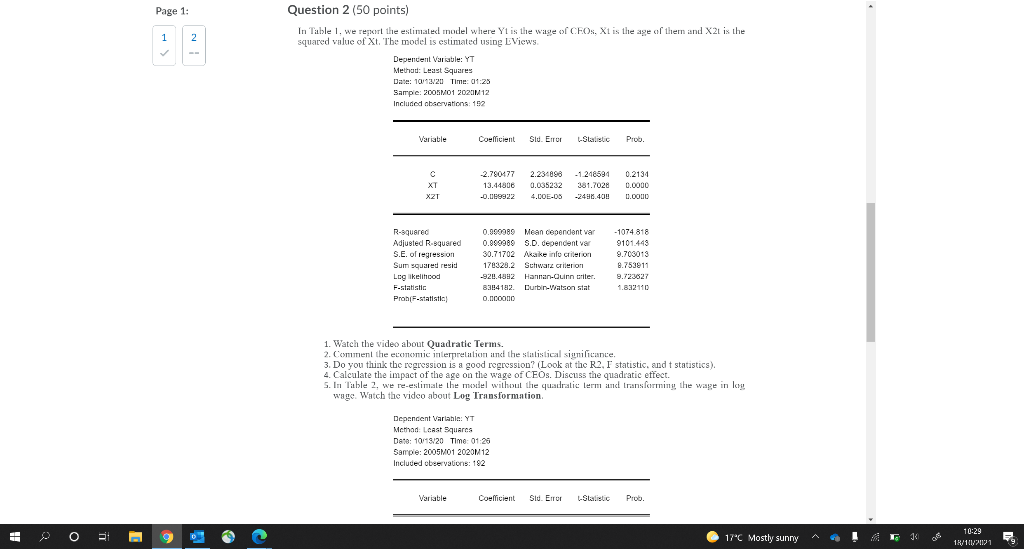

Question: Please do 6,7 Dependent Variable: YT Method: Least Squares Date: 10/13/20 Time: 01:26 Sample: 2005M01 2020M12 Included observations: 192 Variable Coefficient Std. Error t-Statistic Prob.

Please do 6,7

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock