Question: PLEASE, DO NOT COPY AND PASTE ANY ANSWER FROM OTHER CHEGG POSTS Please show me all work so I can learn. Thanks! The table below

PLEASE, DO NOT COPY AND PASTE ANY ANSWER FROM OTHER CHEGG POSTS

Please show me all work so I can learn. Thanks!

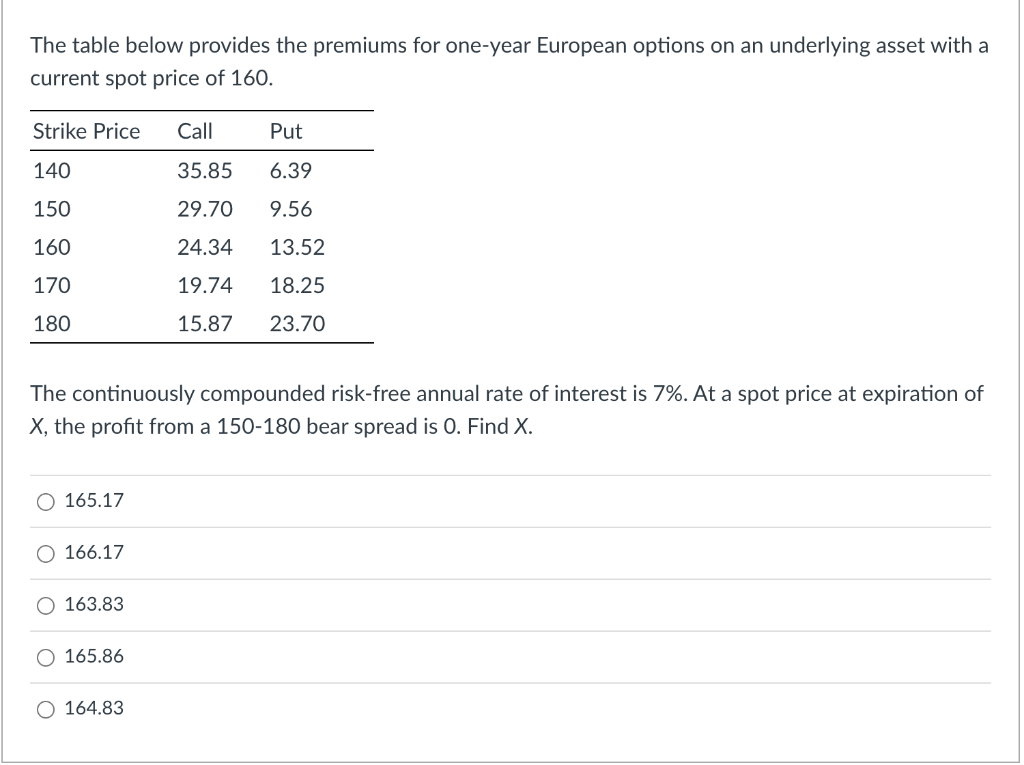

The table below provides the premiums for one-year European options on an underlying asset with a current spot price of 160. Strike Price Call Put 140 35.85 6.39 150 29.70 9.56 160 24.34 13.52 170 19.74 18.25 180 15.87 23.70 The continuously compounded risk-free annual rate of interest is 7%. At a spot price at expiration of X, the profit from a 150-180 bear spread is O. Find X. 165.17 O 166.17 O 163.83 0165.86 O 164.83

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock