Question: Please do not show or use excel, thank you. Problem 9. [8 pts] You are evaluating the performance of two portfolio managers and you have

Please do not show or use excel, thank you.

Please do not show or use excel, thank you.

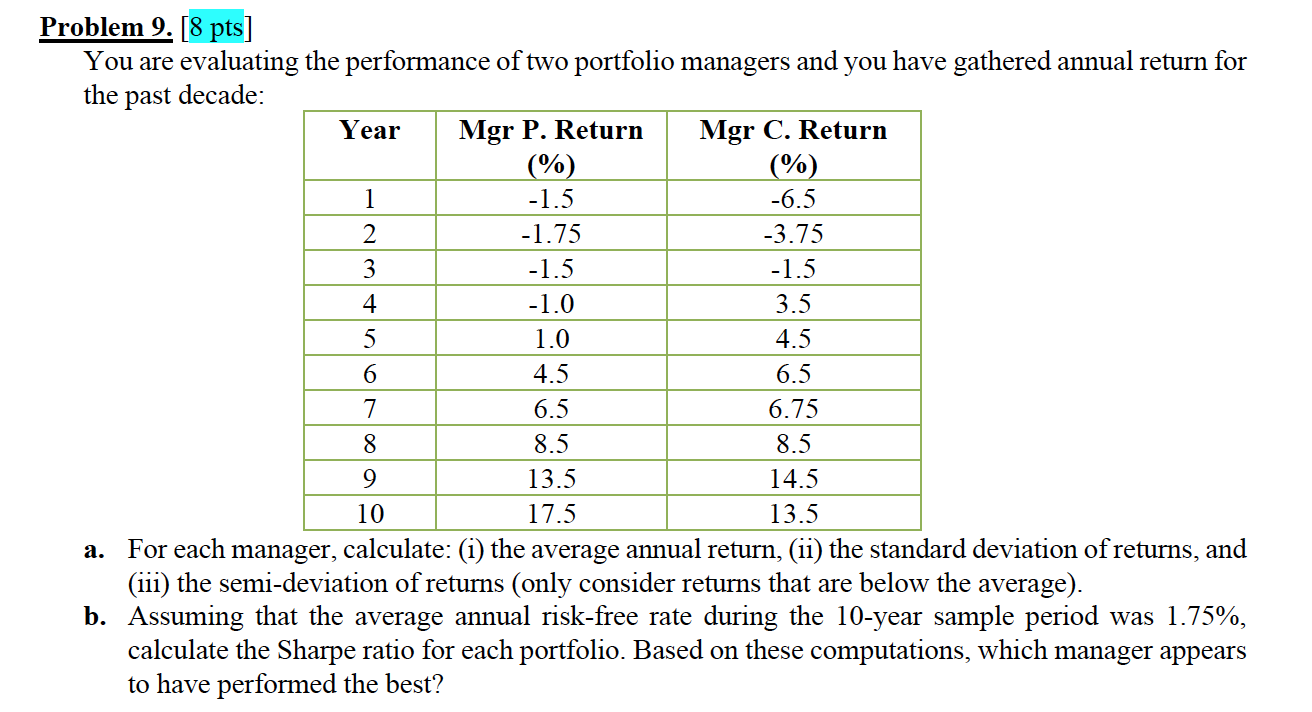

Problem 9. [8 pts] You are evaluating the performance of two portfolio managers and you have gathered annual return for the past decade: Year Mgr P. Return Mgr C. Return (%) (%) 1 -1.5 -6.5 2 -1.75 -3.75 3 -1.5 -1.5 4 -1.0 3.5 5 1.0 4.5 6 4.5 6.5 7 6.5 6.75 8 8.5 8.5 9 13.5 14.5 10 17.5 13.5 a. For each manager, calculate: (i) the average annual return, (ii) the standard deviation of returns, and (iii) the semi-deviation of returns (only consider returns that are below the average). b. Assuming that the average annual risk-free rate during the 10-year sample period was 1.75%, calculate the Sharpe ratio for each portfolio. Based on these computations, which manager appears to have performed the best

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts