Question: Please do not use spreadsheet for calculation K1 K2 Problem 2. (8 pts) Suppose that in the financial market there are two risky stocks S

Please do not use spreadsheet for calculation

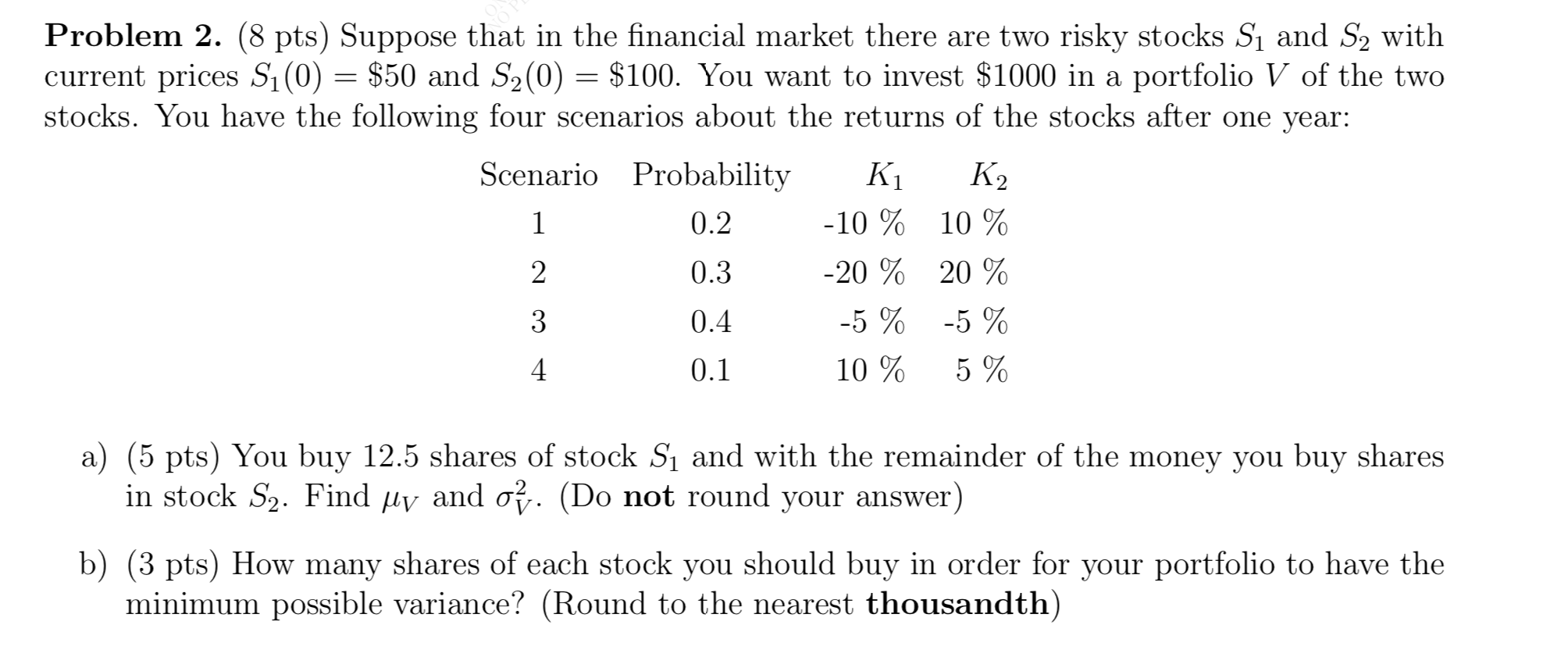

K1 K2 Problem 2. (8 pts) Suppose that in the financial market there are two risky stocks S and S2 with current prices Si(0) = $50 and S2(0) = $100. You want to invest $1000 in a portfolio V of the two stocks. You have the following four scenarios about the returns of the stocks after one year: Scenario Probability 1 0.2 -10 % 10 % 2 0.3 -20% 20% 3 0.4 -5 % -5% 4 0.1 10 % 5 % a) (5 pts) You buy 12.5 shares of stock S and with the remainder of the money you buy shares in stock S2. Find My and oi. (Do not round your answer) b) (3 pts) How many shares of each stock you should buy in order for your portfolio to have the minimum possible variance? (Round to the nearest thousandth) K1 K2 Problem 2. (8 pts) Suppose that in the financial market there are two risky stocks S and S2 with current prices Si(0) = $50 and S2(0) = $100. You want to invest $1000 in a portfolio V of the two stocks. You have the following four scenarios about the returns of the stocks after one year: Scenario Probability 1 0.2 -10 % 10 % 2 0.3 -20% 20% 3 0.4 -5 % -5% 4 0.1 10 % 5 % a) (5 pts) You buy 12.5 shares of stock S and with the remainder of the money you buy shares in stock S2. Find My and oi. (Do not round your answer) b) (3 pts) How many shares of each stock you should buy in order for your portfolio to have the minimum possible variance? (Round to the nearest thousandth)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts