Question: please explain thank you. Consider a complete one-period model with ohm = {omega_1, omega_2, omega_3, omega_4} and let V^1 V^2, V^3, V^4 denote the Arrow-Debreu

please explain

thank you.

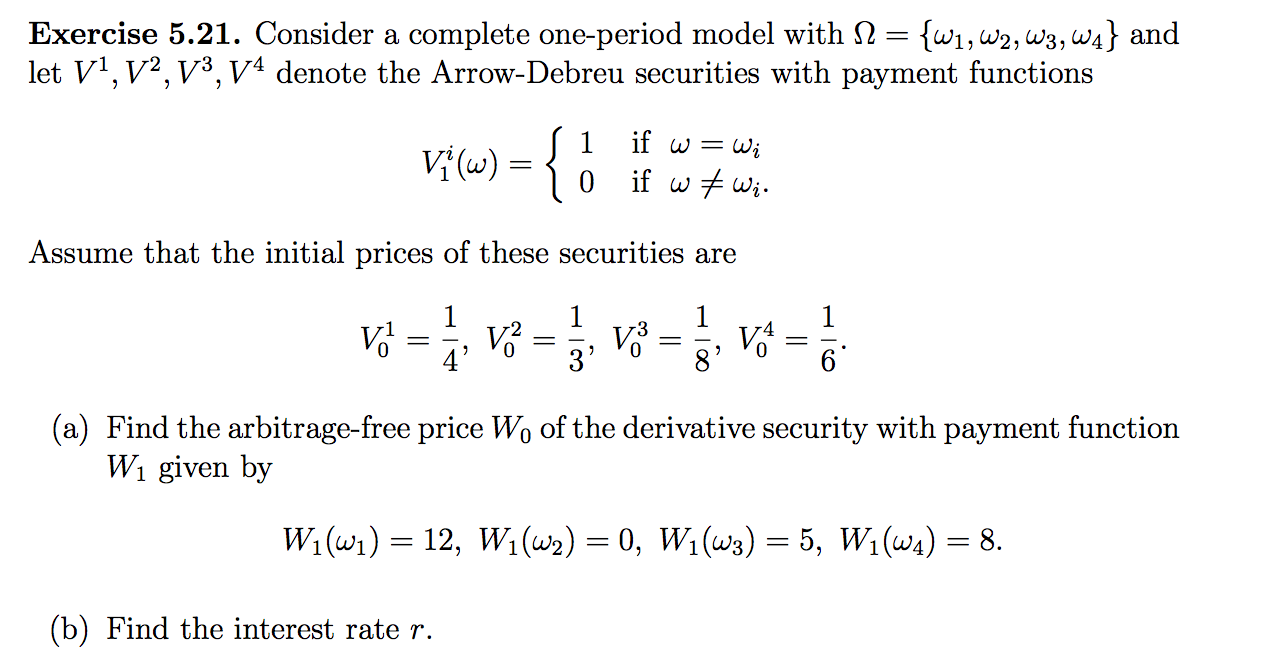

Consider a complete one-period model with ohm = {omega_1, omega_2, omega_3, omega_4} and let V^1 V^2, V^3, V^4 denote the Arrow-Debreu securities with payment functions V^i_1(omega) = {1 if omega = omega_i 0 if omega not equal to omega_i Assume that the initial prices of these securities are V^1_0 = 1/4, V^2_0 = 1/3, V^3_0 = 1/8, V^4_0 = 1/6. Find the arbitrage-free price W_0 of the derivative security with payment function W_1 given by W_1(omega_1) = 12, W_1(omega_2) = 0, W_1(omega_3) = 5, W_1(omega_4) = 8. Find the interest rate r. Consider a complete one-period model with ohm = {omega_1, omega_2, omega_3, omega_4} and let V^1 V^2, V^3, V^4 denote the Arrow-Debreu securities with payment functions V^i_1(omega) = {1 if omega = omega_i 0 if omega not equal to omega_i Assume that the initial prices of these securities are V^1_0 = 1/4, V^2_0 = 1/3, V^3_0 = 1/8, V^4_0 = 1/6. Find the arbitrage-free price W_0 of the derivative security with payment function W_1 given by W_1(omega_1) = 12, W_1(omega_2) = 0, W_1(omega_3) = 5, W_1(omega_4) = 8. Find the interest rate r

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts