Question: Please explain the steps to get the solutions. A non-dividend paying stock, currently priced at 220, is expected to go up by 10% or go

Please explain the steps to get the solutions.

Please explain the steps to get the solutions.

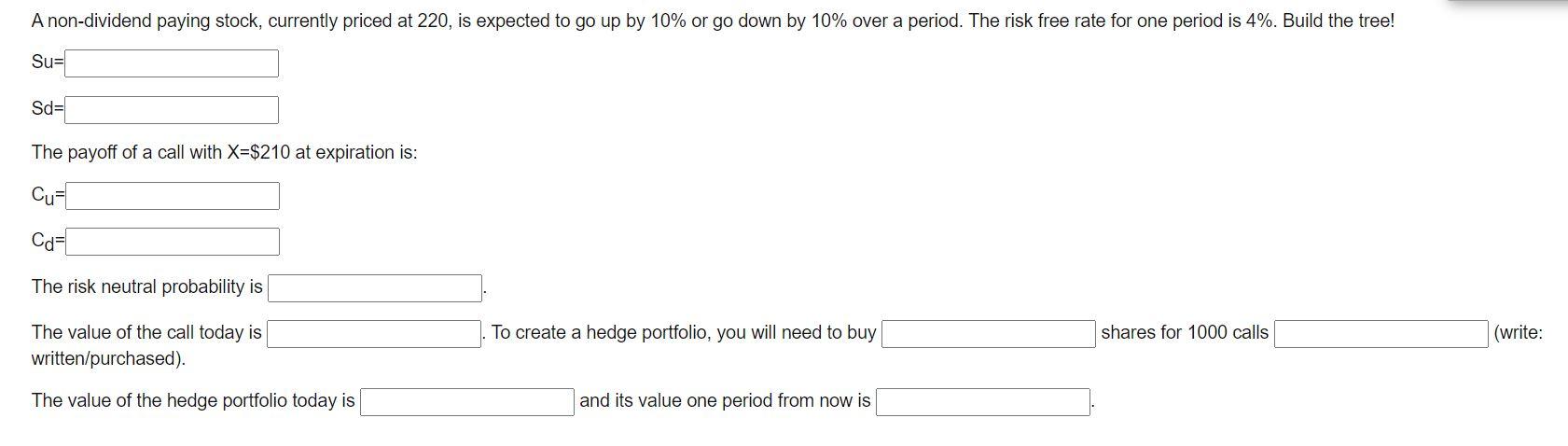

A non-dividend paying stock, currently priced at 220, is expected to go up by 10% or go down by 10% over a period. The risk free rate for one period is 4%. Build the tree! Sur Sd= The payoff of a call with X=$210 at expiration is: Cu= Car The risk neutral probability is To create a hedge portfolio, you will need to buy shares for 1000 calls (write: The value of the call today is written/purchased). The value of the hedge portfolio today is and its value one period from now is A non-dividend paying stock, currently priced at 220, is expected to go up by 10% or go down by 10% over a period. The risk free rate for one period is 4%. Build the tree! Sur Sd= The payoff of a call with X=$210 at expiration is: Cu= Car The risk neutral probability is To create a hedge portfolio, you will need to buy shares for 1000 calls (write: The value of the call today is written/purchased). The value of the hedge portfolio today is and its value one period from now is

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts