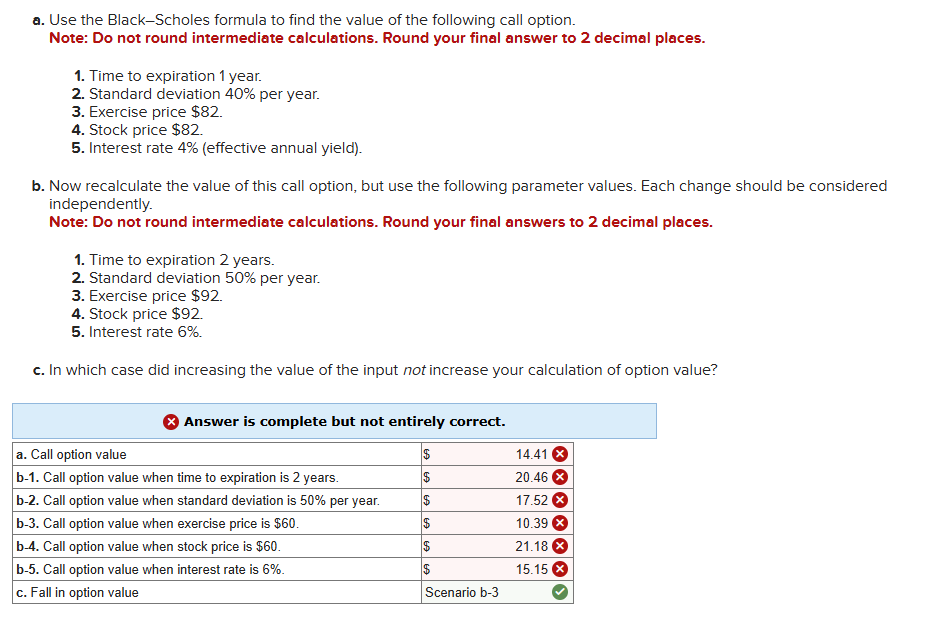

Question: Please fix the errors in the screenshot. Use the Black Scholes formula to find the value of the following call option. Note: Do not round

Please fix the errors in the screenshot. Use the BlackScholes formula to find the value of the following call option.

Note: Do not round intermediate calculations. Round your final answer to decimal places.

Time to expiration year.

Standard deviation per year.

Exercise price $

Stock price $

Interest rate effective annual yield

Now recalculate the value of this call option, but use the following parameter values. Each change should be considered independently.

Note: Do not round intermediate calculations. Round your final answers to decimal places.

Time to expiration years.

Standard deviation per year.

Exercise price $

Stock price $

Interest rate

In which case did increasing the value of the input not increase your calculation of option value?

a Use the BlackScholes formula to find the value of the following call option.

Note: Do not round intermediate calculations. Round your final answer to decimal places.

Time to expiration year.

Standard deviation per year.

Exercise price $

Stock price $

Interest rate effective annual yield

b Now recalculate the value of this call option, but use the following parameter values. Each change should be considered

independently.

Note: Do not round intermediate calculations. Round your final answers to decimal places.

Time to expiration years.

Standard deviation per year.

Exercise price $

Stock price $

Interest rate

c In which case did increasing the value of the input not increase your calculation of option value?

Answer is complete but not entirely correct.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock