Question: Please help and show work how to do it!! Problem 28 points) An FI has a $250 million asset portfolio that has an average duration

Please help and show work how to do it!!

Please help and show work how to do it!!

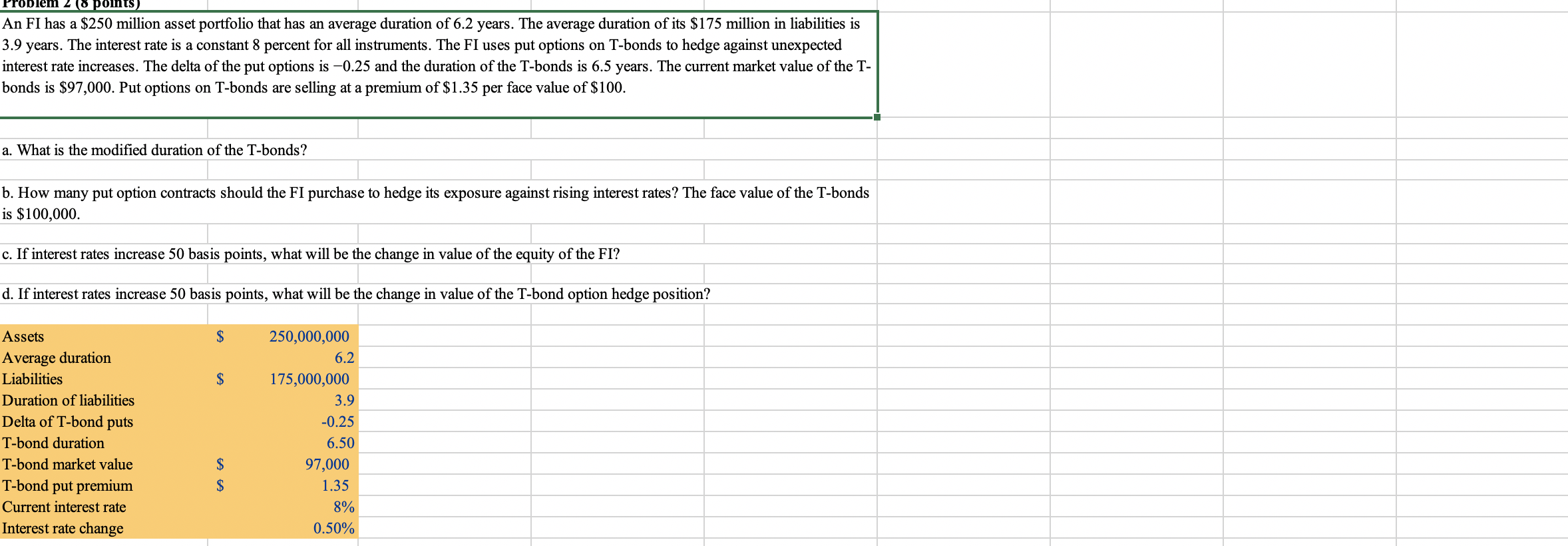

Problem 28 points) An FI has a $250 million asset portfolio that has an average duration of 6.2 years. The average duration of its $175 million in liabilities is 3.9 years. The interest rate is a constant 8 percent for all instruments. The FI uses put options on T-bonds to hedge against unexpected interest rate increases. The delta of the put options is -0.25 and the duration of the T-bonds is 6.5 years. The current market value of the T- bonds is $97,000. Put options on T-bonds are selling at a premium of $1.35 per face value of $100. a. What is the modified duration of the T-bonds? b. How many put option contracts should the FI purchase to hedge its exposure against rising interest rates? The face value of the T-bonds is $100,000. c. If interest rates increase 50 basis points, what will be the change in value of the equity of the FI? d. If interest rates increase 50 basis points, what will be the change in value of the T-bond option hedge position? $ $ Assets Average duration Liabilities Duration of liabilities Delta of T-bond puts T-bond duration T-bond market value T-bond put premium Current interest rate Interest rate change 250,000,000 6.2 175,000,000 3.9 -0.25 6.50 97,000 1.35 8% $ $ 0.50% Problem 28 points) An FI has a $250 million asset portfolio that has an average duration of 6.2 years. The average duration of its $175 million in liabilities is 3.9 years. The interest rate is a constant 8 percent for all instruments. The FI uses put options on T-bonds to hedge against unexpected interest rate increases. The delta of the put options is -0.25 and the duration of the T-bonds is 6.5 years. The current market value of the T- bonds is $97,000. Put options on T-bonds are selling at a premium of $1.35 per face value of $100. a. What is the modified duration of the T-bonds? b. How many put option contracts should the FI purchase to hedge its exposure against rising interest rates? The face value of the T-bonds is $100,000. c. If interest rates increase 50 basis points, what will be the change in value of the equity of the FI? d. If interest rates increase 50 basis points, what will be the change in value of the T-bond option hedge position? $ $ Assets Average duration Liabilities Duration of liabilities Delta of T-bond puts T-bond duration T-bond market value T-bond put premium Current interest rate Interest rate change 250,000,000 6.2 175,000,000 3.9 -0.25 6.50 97,000 1.35 8% $ $ 0.50%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts