Question: Please help answer this question with work/steps included! Problem 1. Consider a stock S paying no dividends, with initial price S(0 S90. European options on

Please help answer this question with work/steps included!

Please help answer this question with work/steps included!

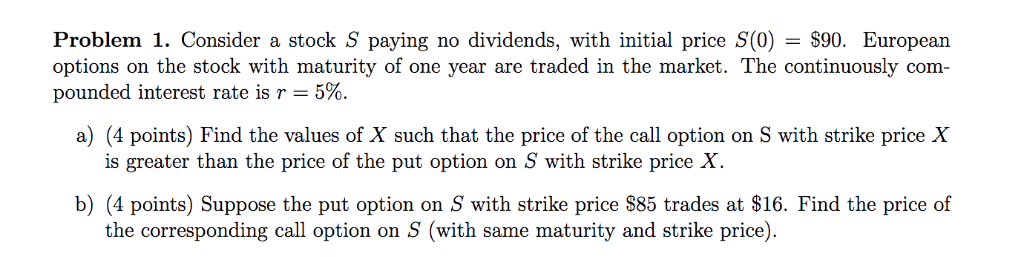

Problem 1. Consider a stock S paying no dividends, with initial price S(0 S90. European options on the stock with maturity of one year are traded in the market. The continuously com- a) (4 points) Find the values of X such that the price of the call option on S with strike price X b) (4 points) Suppose the put option on S with strike price S85 trades at $16. Find the price of 5%. pounded interest rate is r man is greater than the price of the put option on S with strike price X the corresponding call option on S (with same maturity and strike price)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock