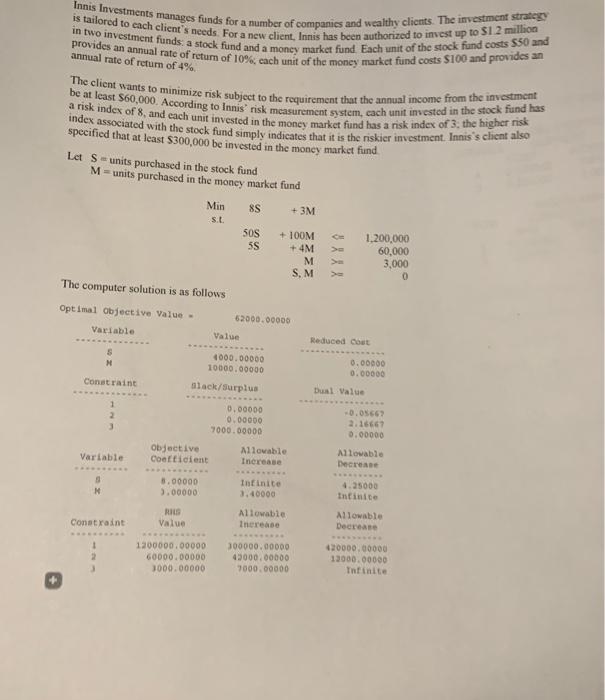

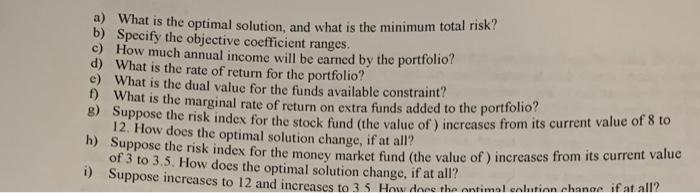

Question: Please help is tailored to each client's needs. For a new client. Innis has been authorized to invest up to $1.2 million in two investment

Please help

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock