Question: Please help LI C n 9. Value-at-Risk (VaR) Statistic (LO4, CFA6) Your portfolio allocates equal funds to the DW Co. and Woodpecker, Inc., stocks referred

Please help

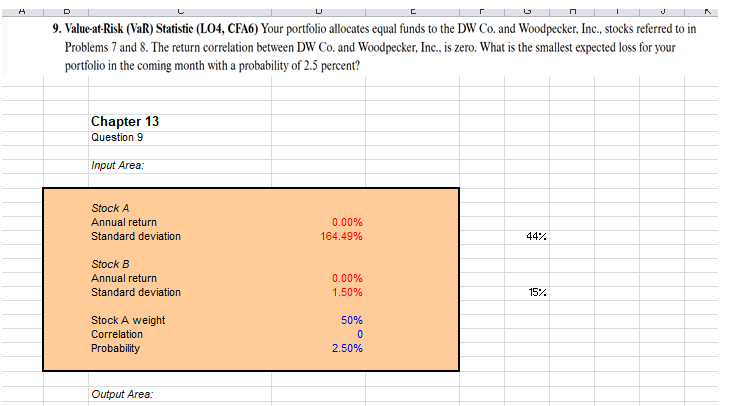

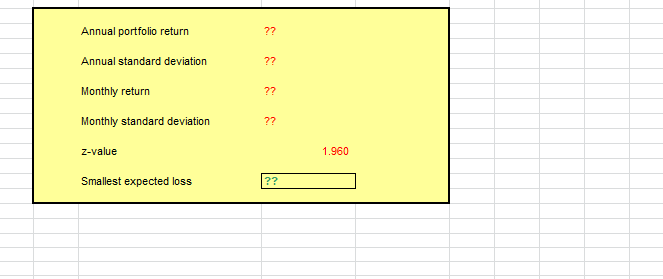

LI C n 9. Value-at-Risk (VaR) Statistic (LO4, CFA6) Your portfolio allocates equal funds to the DW Co. and Woodpecker, Inc., stocks referred to in Problems 7 and 8. The return correlation between DW Co. and Woodpecker, Inc., is zero. What is the smallest expected loss for your portfolio in the coming month with a probability of 2.5 percent? Chapter 13 Question 9 Input Area: Stock A Annual return 0.00% Standard deviation 164.49% 44% Stock B Annual return 0.00% Standard deviation 1.50% 15% Stock A weight 50% Correlation Probability 2.50% Output Area:Annual portfolio return ?? Annual standard deviation ?? Monthly return ?? Monthly standard deviation ?? z-value 1.960 Smallest expected loss

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts