Question: please help. make balance sheet and income statement a) The January 31 2021 bank statement showed that a cash deposit was incorrectly posted as $270

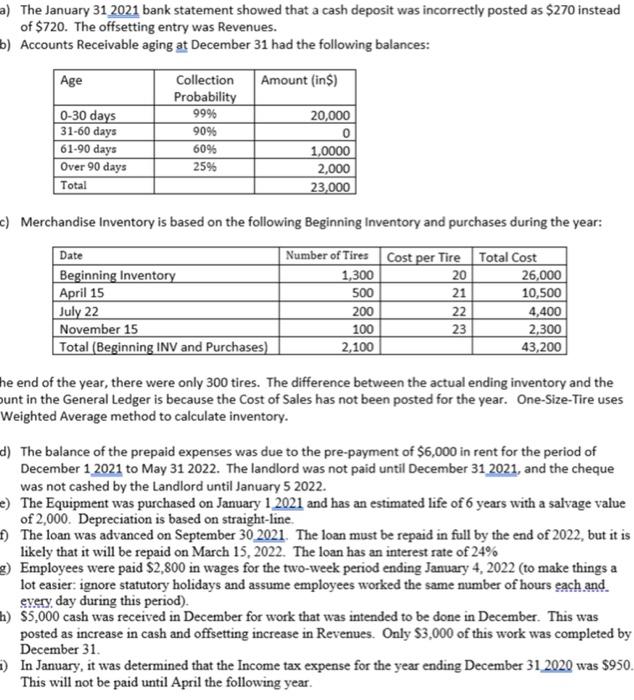

a) The January 31 2021 bank statement showed that a cash deposit was incorrectly posted as $270 instead of $720. The offsetting entry was Revenues. b) Accounts Receivable aging at December 31 had the following balances: Age Amount (ins) Collection Probability 99% 90% 60% 25% 0-30 days 31-60 days 61.90 days Over 90 days Total 20,000 1,0000 2,000 23,000 c) Merchandise Inventory is based on the following Beginning Inventory and purchases during the year: Date Number of Tires Cost per Tire Total Cost Beginning Inventory 1,300 20 26,000 April 15 500 10,500 July 22 200 22 4,400 November 15 100 23 2,300 Total (Beginning INV and Purchases) 2,100 43,200 21 he end of the year, there were only 300 tires. The difference between the actual ending inventory and the sunt in the General Ledger is because the cost of Sales has not been posted for the year. One-Size-Tire uses Weighted Average method to calculate inventory. d) The balance of the prepaid expenses was due to the pre-payment of $6,000 in rent for the period of December 1 2021 to May 31 2022. The landlord was not paid until December 31 2021, and the cheque was not cashed by the Landlord until January 5 2022. e) The Equipment was purchased on January 1 2021 and has an estimated life of 6 years with a salvage value of 2,000. Depreciation is based on straight-line. The loan was advanced on September 30 2021. The loan must be repaid in full by the end of 2022, but it is likely that it will be repaid on March 15, 2022. The loan has an interest rate of 24% g) Employees were paid $2,800 in wages for the two-week period ending January 4, 2022 (to make things a lot easier: ignore statutory holidays and assume employees worked the same number of hours each and every day during this period). h) $5,000 cash was received in December for work that was intended to be done in December. This was posted as increase in cash and offsetting increase in Revenues. Only $3,000 of this work was completed by December 31. In January, it was determined that the Income tax expense for the year ending December 31 2020 was $950. This will not be paid until April the following year. a) The January 31 2021 bank statement showed that a cash deposit was incorrectly posted as $270 instead of $720. The offsetting entry was Revenues. b) Accounts Receivable aging at December 31 had the following balances: Age Amount (ins) Collection Probability 99% 90% 60% 25% 0-30 days 31-60 days 61.90 days Over 90 days Total 20,000 1,0000 2,000 23,000 c) Merchandise Inventory is based on the following Beginning Inventory and purchases during the year: Date Number of Tires Cost per Tire Total Cost Beginning Inventory 1,300 20 26,000 April 15 500 10,500 July 22 200 22 4,400 November 15 100 23 2,300 Total (Beginning INV and Purchases) 2,100 43,200 21 he end of the year, there were only 300 tires. The difference between the actual ending inventory and the sunt in the General Ledger is because the cost of Sales has not been posted for the year. One-Size-Tire uses Weighted Average method to calculate inventory. d) The balance of the prepaid expenses was due to the pre-payment of $6,000 in rent for the period of December 1 2021 to May 31 2022. The landlord was not paid until December 31 2021, and the cheque was not cashed by the Landlord until January 5 2022. e) The Equipment was purchased on January 1 2021 and has an estimated life of 6 years with a salvage value of 2,000. Depreciation is based on straight-line. The loan was advanced on September 30 2021. The loan must be repaid in full by the end of 2022, but it is likely that it will be repaid on March 15, 2022. The loan has an interest rate of 24% g) Employees were paid $2,800 in wages for the two-week period ending January 4, 2022 (to make things a lot easier: ignore statutory holidays and assume employees worked the same number of hours each and every day during this period). h) $5,000 cash was received in December for work that was intended to be done in December. This was posted as increase in cash and offsetting increase in Revenues. Only $3,000 of this work was completed by December 31. In January, it was determined that the Income tax expense for the year ending December 31 2020 was $950. This will not be paid until April the following year

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts