Question: Please help me. QUESTION 1 Consider the following regression model, .Vr = 51 ' Bzxrz ' + BKXiK+ 9; where E[ 9: Xi] = 0

Please help me.

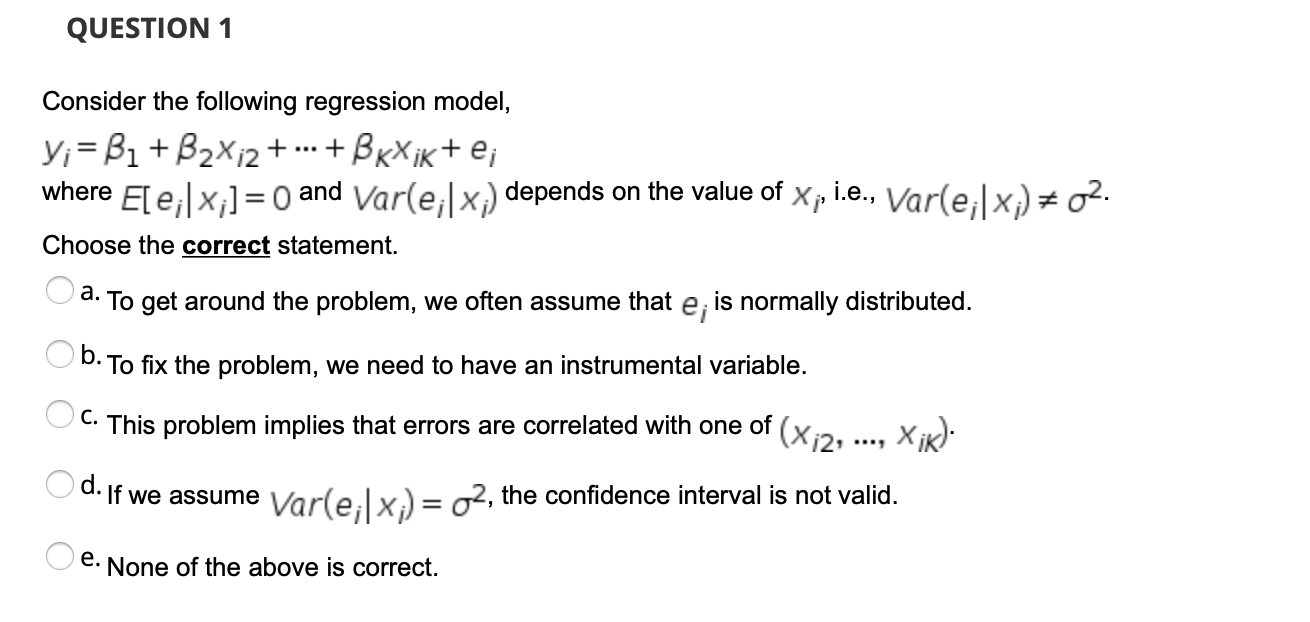

QUESTION 1 Consider the following regression model, .Vr = 51 "' Bzxrz '" + BKXiK+ 9; where E[ 9:" Xi] = 0 and Var(e,| Xi) depends on the value of Xi' i.e., V0r(9i| Xi) ,3 02. Choose the correct statement. A K 7 3 a. To get around the problem, we often assume that e'. is normally distributed. . b' To x the problem, we need to have an instrumental variable. A This problem Implles that errors are correlated With one of (X12: ..., XIX)- ('3 If we assume Va r(9i| Xi) = 02, the condence Interval IS not valid. r\". e . None of the above Is correct

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock