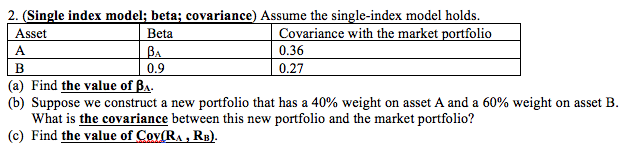

Question: Please help me solve a, b, and c 2. (Single index model; beta; covariance) Assume the single-index model holds Beta Covariance with the market portfolio

Please help me solve a, b, and c

2. (Single index model; beta; covariance) Assume the single-index model holds Beta Covariance with the market portfolio 0.36 0.27 Asset BA i.2 (a) Find the value of BA. (b) Suppose we construct a new portfolio that has a 40% weight on asset A and a 60% weight on asset B. (c) Find the value of Cov RA, RB). 2 (a) 1.2 (b) 0.306 (c) 0.324

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock