Question: Please help me solve a, b, c, d and e 5. (Currency options: speculation: appreciation) John focuses his time and attention on the U.S dollar/euro

Please help me solve a, b, c, d and e

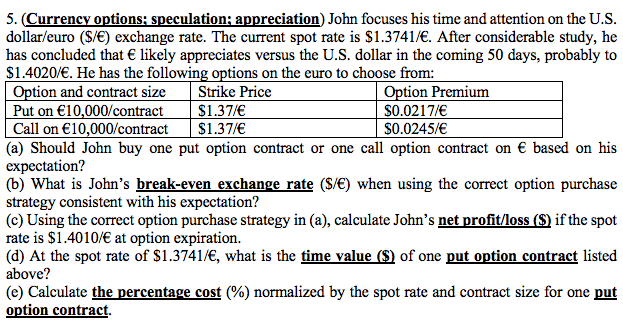

5. (Currency options: speculation: appreciation) John focuses his time and attention on the U.S dollar/euro (S/E) exchange rate. The current spot rate is S1.3741/. After considerable study, he has concluded that likely appreciates versus the U.S. dollar in the coming 50 days, probably to $1.4020/E. He has the following options on the euro to choose from: tion and contract size Strike Price Put on 10,000/contract $1.37/ Call on 10,000/contract S1.37/ (a) Should John buy one put option contract or one call option contract on based on his expectation? (b) What is John's break-even exchange rate (S/) when using the correct option purchase strategy consistent with his expectation? (c) Using the correct option purchase strategy in (a), calculate John's net profit/loss (S) if the spot rate is S1.4010/ at option expiration. (d) At the spot rate of $1.3741/, what is the time value (S of one put option contract listed above? (e) Calculate the percentage cost (%) normalized by the spot rate and contract size for one put option contract tion Premium 0.0217e S0.0245/ 5 (a) Buy a call option contract on euros. (b) $1.3945/ (c) $65 (d) $217 (e) 1.58%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts