Question: Please help me solve the problem on 11 and 12! 11) You are a risk-averse investor whose coefficient of risk aversion (A) 2.0. Your risk

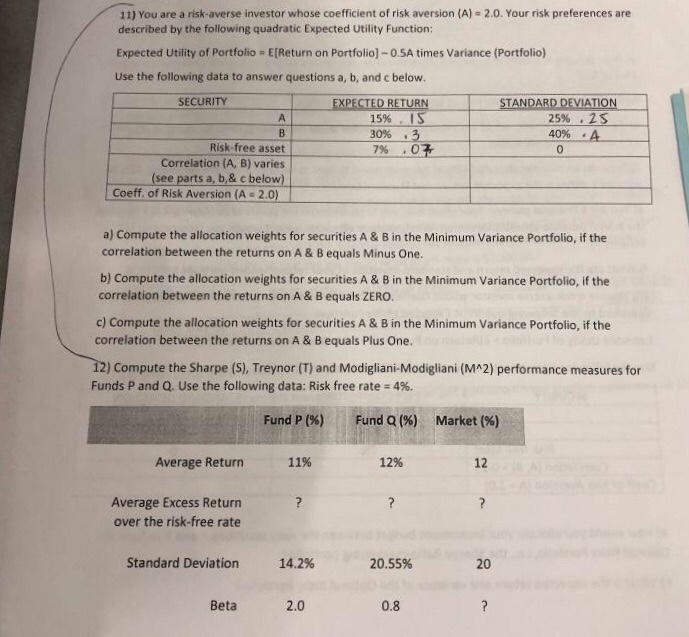

11) You are a risk-averse investor whose coefficient of risk aversion (A) 2.0. Your risk preferences are described by the following quadratic Expected Utility Function: Expected Utility of Portfolio = E [Return on Portfolio-0.5A times variance (Portfolio) Use the following data to answer questions a, b, and c below. SECURITY STANDARDDEVIATION 15%(11 30% - 25% , 2s 40% ia Risk-free asset Correlation (A, B) varies (see parts a, b,& c below) 0 Coeff. of Risk Aversion (A 2.0) a) Compute the allocation weights for securities A & B in the Minimum Variance Portfolio, if the correlation between the returns on A & B equals Minus One. b) Compute the allocation weights for securities A & B in the Minimum Variance Portfolio, if the correlation between the returns on A & B equals ZERO. c) Compute the allocation weights for securities A & B in the Minimum Variance Portfolio, if the correlation between the returns on A & B equals Plus One. ) Compute the Sharpe (S), Treynor (T) and Modigliani-Modigliani (MA2) performance measures for Funds P and Q. Use the following data: Risk free rate : 4%. Fund P (%) Fund Q (%) Market (%) Average Return 11% 12% 12 Average Excess Return over the risk-free rate Standard Deviation 14.2% 20.55% 20 Beta 2.0 0.8

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts