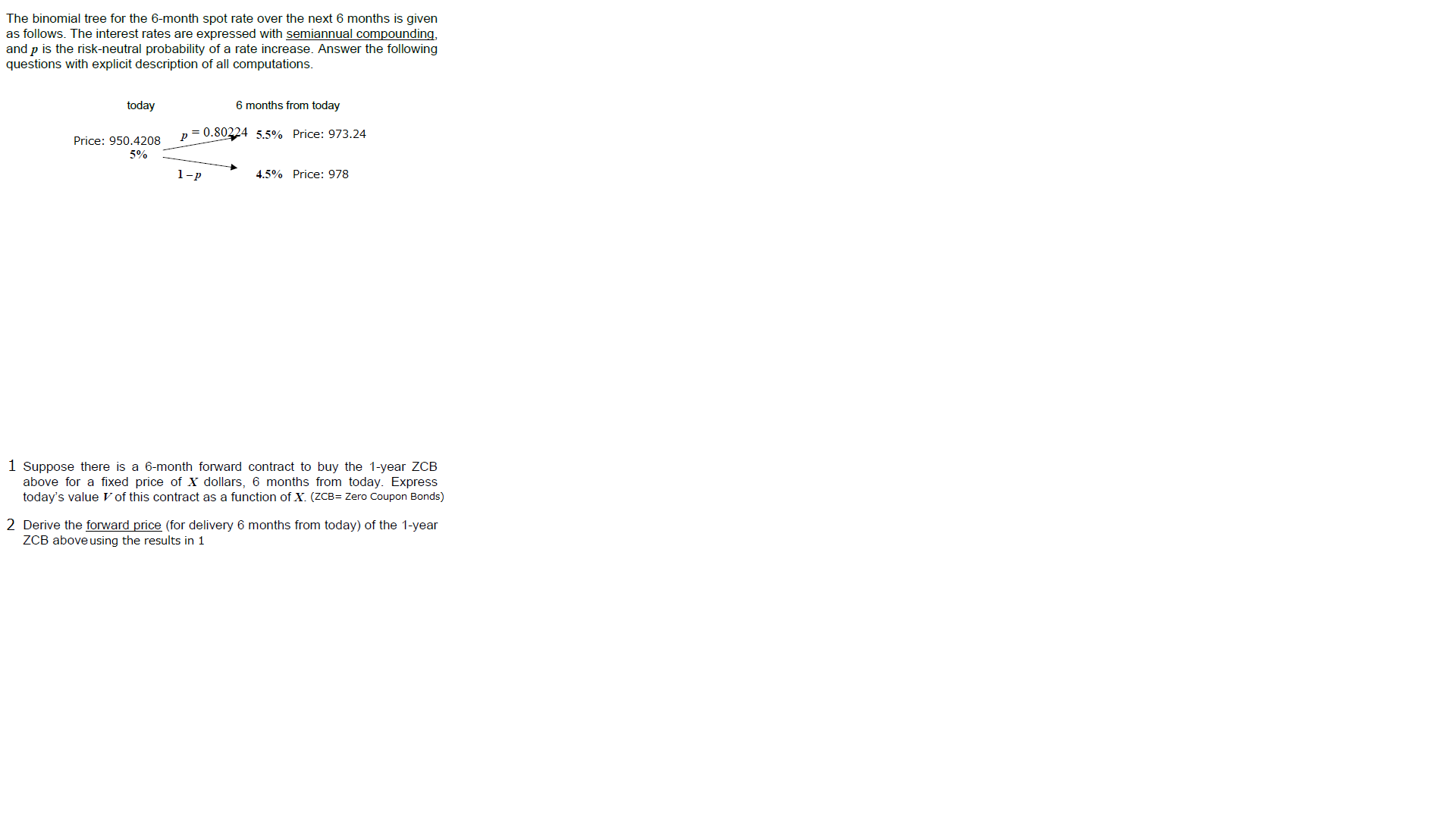

Question: Please help me to answer this The binomial tree for the 6-month spot rate over the next 6 months is given as follows. The interest

Please help me to answer this

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock