Question: please help please help Question Two [Total 19 Marks] Shown below is the statement of financial position dated 31 December 2020 for Ndiyepano Ltd, a

![please help please help Question Two [Total 19 Marks] Shown below](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2024/09/66edba40eff07_74466edba4079e75.jpg)

please help

please help

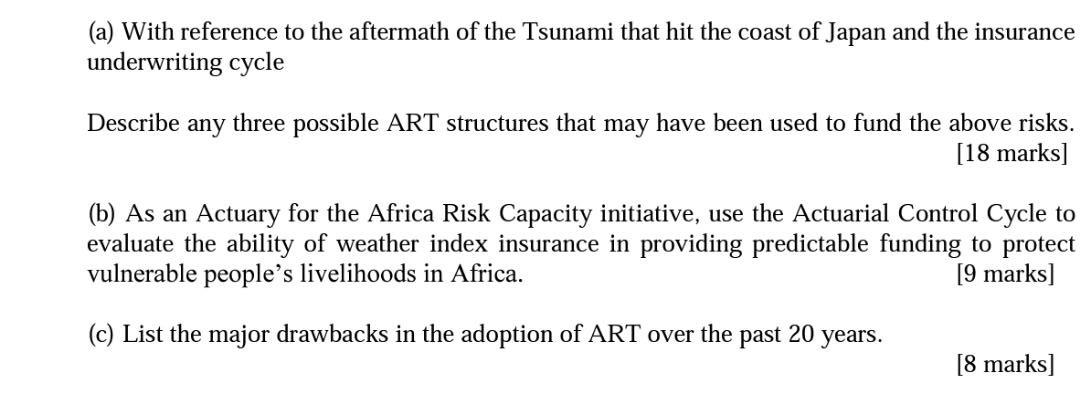

Question Two [Total 19 Marks] Shown below is the statement of financial position dated 31 December 2020 for Ndiyepano Ltd, a metal fabrication company. ASSETS K K Non-current assets Factory Machinery 6,750,000 1,250,000 8,000,000 Current assets Inventories 850,000 Trade receivables. 250,000 Cash 400,000 1,500,000 Total assets 9,500,000 EQUITY AND LIABILITIES 2,500,000 Issued ordinary shares of K5 Other reserves: Share premium account Revaluation reserve 1,800,000 870,000 Retained earnings Total equity 5,170,000 Non-current liabilities 8% Convertible loan stock 2025 2,000,000 10% Debentures 2029 1,500,000 3,500,000 Current liabilities Trade payables 340,000 Bank loan 300,000 Tax payable 190,000 830,000 Total liabilities 4,330,000 Total equity and liabilities 9,500,000 During 2021, the following occurred: K sales 5,550,000 Increase in inventories 170,000 1,120.000 purchases of raw materials staff costs 850,000 electricity costs. 910,000 advertising and delivery costs. 590.000 cash payments received 4,470,000 Increase in trade payables. 250,000 dividends paid 120,000 tax paid 130,000 390,000 increase in cash You are also given the following information: (a) The company repaid its bank loan on 5 January 2021. (b) The factory was originally purchased in December 2009. In 2020 it was revalued and its remaining life estimated to be 10 years at which time it would be worth zero. The annual depreciation charge for 2020 was based on the revalued figure and the revaluation of the factory was included in the 2020 revaluation reserve. The machinery was purchased in 20120 for a price of K1,500,000. It is being depreciated to zero over a period of six years. (c) The first conversion date for the 8% CULS was 15 December 2015. K1,000,000 nominal was converted. The conversion terms were 2 shares for every K50 nominal of convertible stock. Interest was paid before conversion took place. (d) The directors were concerned about the level of trade receivables and decided to set up a provision for bad debts equal to 10% of the trade receivables outstanding at the end of the accounting year. Assuming a tax rate of 20%, draw up the statement of comprehensive income for 2021 and the statement of financial position dated 31 December 2021 in a form suitable for publication. [19 marks] 1,000,000 800,000 (a) With reference to the aftermath of the Tsunami that hit the coast of Japan and the insurance underwriting cycle Describe any three possible ART structures that may have been used to fund the above risks. [18 marks] (b) As an Actuary for the Africa Risk Capacity initiative, use the Actuarial Control Cycle to evaluate the ability of weather index insurance in providing predictable funding to protect vulnerable people's livelihoods in Africa. [9 marks] (c) List the major drawbacks in the adoption of ART over the past 20 years. [8 marks] Question Two [Total 19 Marks] Shown below is the statement of financial position dated 31 December 2020 for Ndiyepano Ltd, a metal fabrication company. ASSETS K K Non-current assets Factory Machinery 6,750,000 1,250,000 8,000,000 Current assets Inventories 850,000 Trade receivables. 250,000 Cash 400,000 1,500,000 Total assets 9,500,000 EQUITY AND LIABILITIES 2,500,000 Issued ordinary shares of K5 Other reserves: Share premium account Revaluation reserve 1,800,000 870,000 Retained earnings Total equity 5,170,000 Non-current liabilities 8% Convertible loan stock 2025 2,000,000 10% Debentures 2029 1,500,000 3,500,000 Current liabilities Trade payables 340,000 Bank loan 300,000 Tax payable 190,000 830,000 Total liabilities 4,330,000 Total equity and liabilities 9,500,000 During 2021, the following occurred: K sales 5,550,000 Increase in inventories 170,000 1,120.000 purchases of raw materials staff costs 850,000 electricity costs. 910,000 advertising and delivery costs. 590.000 cash payments received 4,470,000 Increase in trade payables. 250,000 dividends paid 120,000 tax paid 130,000 390,000 increase in cash You are also given the following information: (a) The company repaid its bank loan on 5 January 2021. (b) The factory was originally purchased in December 2009. In 2020 it was revalued and its remaining life estimated to be 10 years at which time it would be worth zero. The annual depreciation charge for 2020 was based on the revalued figure and the revaluation of the factory was included in the 2020 revaluation reserve. The machinery was purchased in 20120 for a price of K1,500,000. It is being depreciated to zero over a period of six years. (c) The first conversion date for the 8% CULS was 15 December 2015. K1,000,000 nominal was converted. The conversion terms were 2 shares for every K50 nominal of convertible stock. Interest was paid before conversion took place. (d) The directors were concerned about the level of trade receivables and decided to set up a provision for bad debts equal to 10% of the trade receivables outstanding at the end of the accounting year. Assuming a tax rate of 20%, draw up the statement of comprehensive income for 2021 and the statement of financial position dated 31 December 2021 in a form suitable for publication. [19 marks] 1,000,000 800,000 (a) With reference to the aftermath of the Tsunami that hit the coast of Japan and the insurance underwriting cycle Describe any three possible ART structures that may have been used to fund the above risks. [18 marks] (b) As an Actuary for the Africa Risk Capacity initiative, use the Actuarial Control Cycle to evaluate the ability of weather index insurance in providing predictable funding to protect vulnerable people's livelihoods in Africa. [9 marks] (c) List the major drawbacks in the adoption of ART over the past 20 years. [8 marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts