Question: Please help Question 05 { * 1 How many expected return, variance, and covariance estimates does an active portfolio manager need for 50 assets? B

Please help

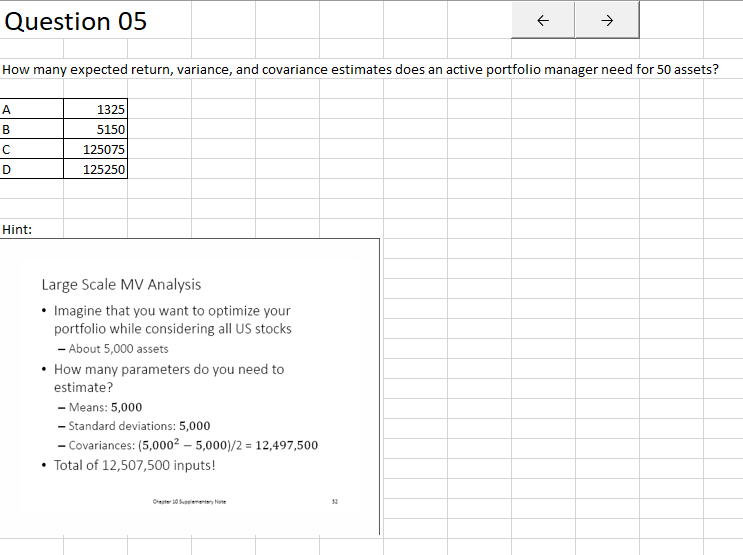

Question 05 { * 1 How many expected return, variance, and covariance estimates does an active portfolio manager need for 50 assets? B 1325 5150 125075 125250 D Hint: Large Scale MV Analysis Imagine that you want to optimize your portfolio while considering all US stocks - About 5,000 assets How many parameters do you need to estimate? - Means: 5,000 - Standard deviations: 5,000 - Covariances: (5,0002 - 5,000)/2 = 12,497,500 Total of 12,507,500 inputs! Crepes Supplementary one

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock