Question: PLEASE HELP QUESTION 2. THE ANSWER I GAVE IS CORRECT Questions 1-8 should be answered by building a 15-period binomial model whose parameters should be

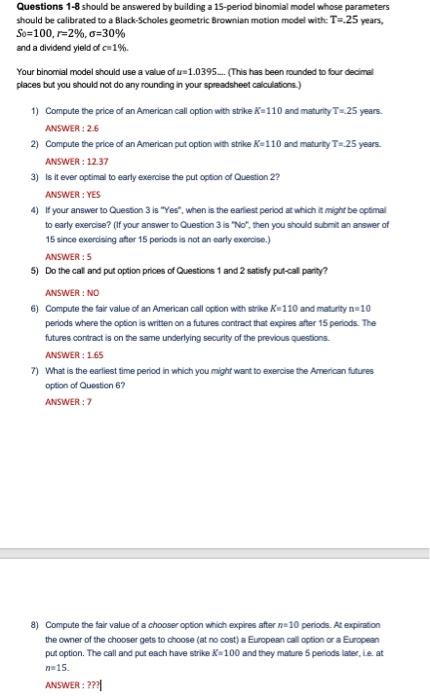

Questions 1-8 should be answered by building a 15-period binomial model whose parameters should be calibrated to a Black-Scholes geometric Brownian motion model with: T= 25 years, So=100,r=2%, o=30% and a dividend yield of c=1% Your binomial model should use a value of u1.0395_. (This has been founded to four decima places but you should not do any rounding in your spreadsheet calculations.) 1) Compute the price of an American call option with strike K=110 and maturityT= 25 years. ANSWER: 2.6 2) Compute the price of an American put option with strike K-110 and maturity T-25 years ANSWER : 12.37 3) Is it ever optimal to early exercise the put option of Question 2? ANSWER: YES 4) If your answer to Question 3 is "Yes", when is the earliest period at which it might be optimal to early exercise? (if your answer to Question 3 is "No", then you should submit an answer of 15 since exercising after 15 periods is not an early exercise.) ANSWER: 5 5) Do the call and put option prices of Questions 1 and 2 satisfy put-cal party? ANSWER: NO 6) Compute the fair value of an American call option with strike K-110 and maturity n=10 periods where the option is written on a futures contract that expires after 15 periods. The futures contract is on the same underlying security of the previous questions ANSWER: 165 7) What is the earliest time period in which you might want to exercise the American fitures option of Question 67 ANSWER: 8) Compute the fair value of a chooser option which expires after n=10 periods. At expiration the owner of the chooser gets to choose (at no cost) a European call option or a European put option. The call and put each have strike X-100 and they mature 5 periods later, Le at na 15

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts