Question: please help Step 1 - You Apply for Credit A is a form or interview that provides information to the lender about your ability and

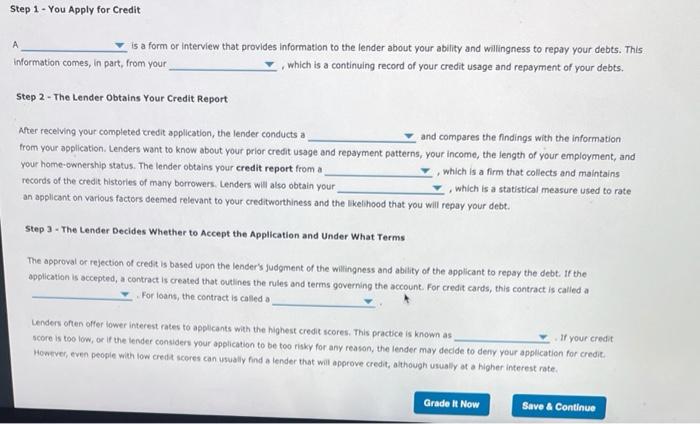

Step 1 - You Apply for Credit A is a form or interview that provides information to the lender about your ability and willingness to repay your debts. This Information comes, in part, from your C, which is a continuing record of your credit usage and repayment of your debts. Step 2 - The Lender Obtains Your Credit Report After receiving your completed credit application, the lender conducts a and compares the findings with the information from your application. Lenders want to know about your prior credit usage and repayment patterns, your income, the length of your employment, and your home-ownership status. The lender obtains your credit report from a which is a firm that collects and maintains records of the credit histories of many borrowers. Lenders will also obtain your which is a statistical measure used to rate an applicant on various factors deemed relevant to your creditworthiness and the likelihood that you will repay your debt. Step 3 - The Lender Decides Whether to accept the Application and Under What Terms The approval or rejection of credit is based upon the lender's judgment of the willingness and ability of the applicant to repay the debt. If the application is accepted, a contract is created that outlines the rules and terms governing the account. For credit cards, this contract is called a For loans, the contract is called a Lenders often offer tower interest rates to applicants with the highest credit scores. This practice is known as If your credit score is too low, or if the tender consider your application to be too risky for any reason, the lender may decide to deny your application for credit. However, even people with low credit scores can usually find a lender that will approve credit, although usually at a higher interest rate Grade it Now Save & Continue Step 1 - You Apply for Credit A is a form or interview that provides information to the lender about your ability and willingness to repay your debts. This Information comes, in part, from your C, which is a continuing record of your credit usage and repayment of your debts. Step 2 - The Lender Obtains Your Credit Report After receiving your completed credit application, the lender conducts a and compares the findings with the information from your application. Lenders want to know about your prior credit usage and repayment patterns, your income, the length of your employment, and your home-ownership status. The lender obtains your credit report from a which is a firm that collects and maintains records of the credit histories of many borrowers. Lenders will also obtain your which is a statistical measure used to rate an applicant on various factors deemed relevant to your creditworthiness and the likelihood that you will repay your debt. Step 3 - The Lender Decides Whether to accept the Application and Under What Terms The approval or rejection of credit is based upon the lender's judgment of the willingness and ability of the applicant to repay the debt. If the application is accepted, a contract is created that outlines the rules and terms governing the account. For credit cards, this contract is called a For loans, the contract is called a Lenders often offer tower interest rates to applicants with the highest credit scores. This practice is known as If your credit score is too low, or if the tender consider your application to be too risky for any reason, the lender may decide to deny your application for credit. However, even people with low credit scores can usually find a lender that will approve credit, although usually at a higher interest rate Grade it Now Save & Continue

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts