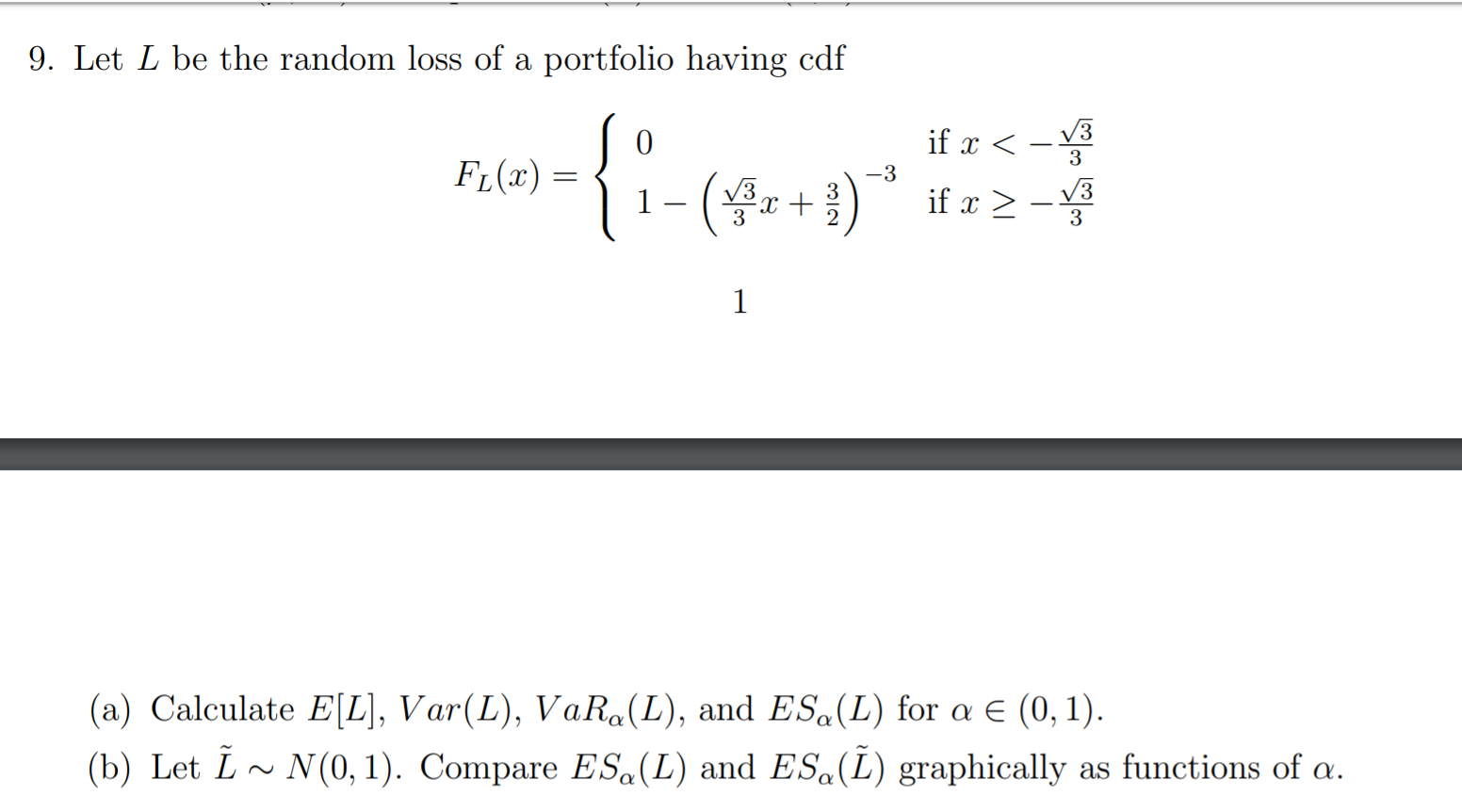

Question: Please help with following: (financial math) 9. Let L be the random loss of a portfolio having cdf if x V3 3 (a) Calculate E[L],

Please help with following: (financial math)

9. Let L be the random loss of a portfolio having cdf if x V3 3 (a) Calculate E[L], Var(L), VaRa( L), and ESa(L) for a E (0, 1). (b) Let L ~ N(0, 1). Compare ESa(L) and ESa(L) graphically as functions of a

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock