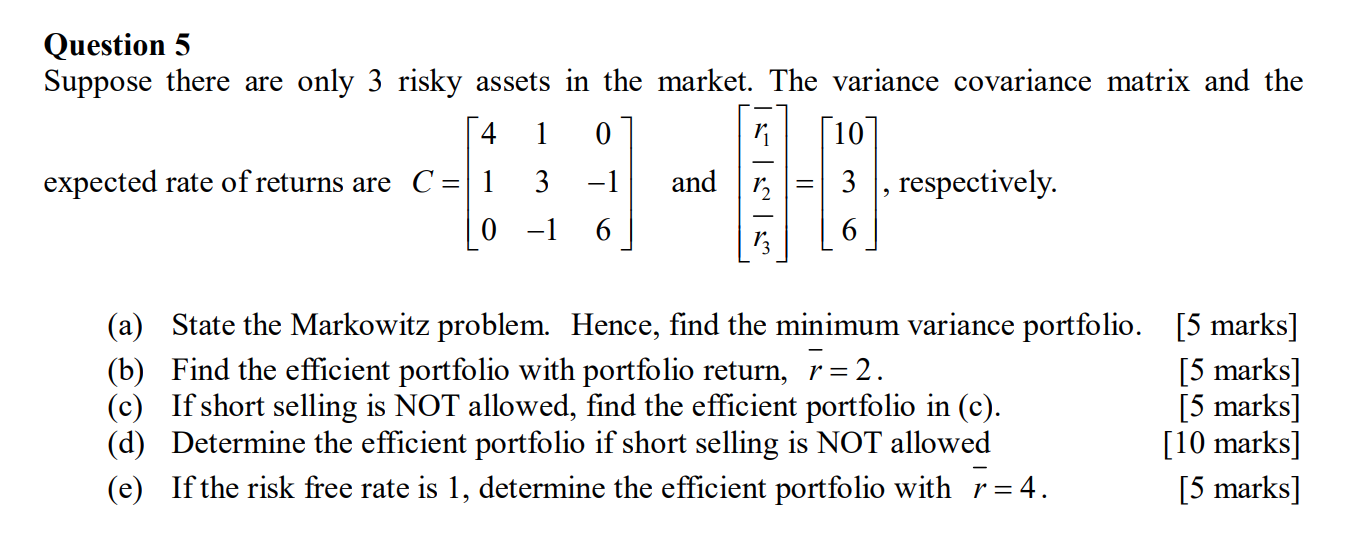

Question: Please help with this question. Thanks Question 5 Suppose there are only 3 risky assets in the market. The variance covariance matrix and the 410

Please help with this question. Thanks

Question 5 Suppose there are only 3 risky assets in the market. The variance covariance matrix and the 410 '110 3 , respectively. expected rate of returns are C = 1 3 1 and r2 0 1 6 13 (a) State the Markowitz problem Hence, nd the minimum variance portfolio. [5 marks] (1)) Find the efficient portfolio with portfolio return, r = 2. [5 marks] (0) If short selling is NOT allowed, nd the efficient portfolio in (c). [5 marks] ((1) Determine the efficient portfolio if short selling is NOT allowed [10 marks] (6) If the risk free rate is 1, determine the efficient portfolio with ;= 4. [5 marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts