Question: Please help with this question Tron Corp. was authorized to issue $500,000 of face value bonds, as follows: Date of Interest authorization Term rate Interest

Please help with this question

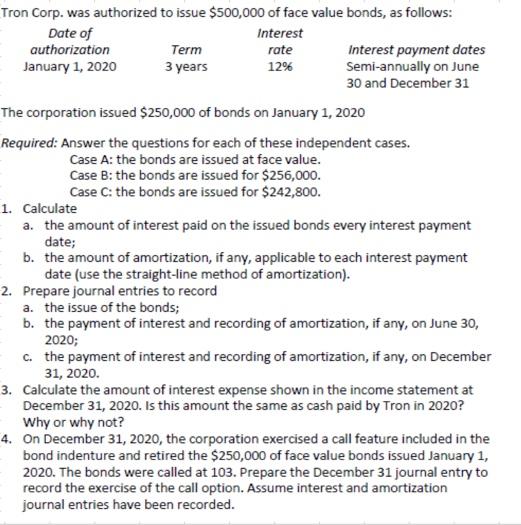

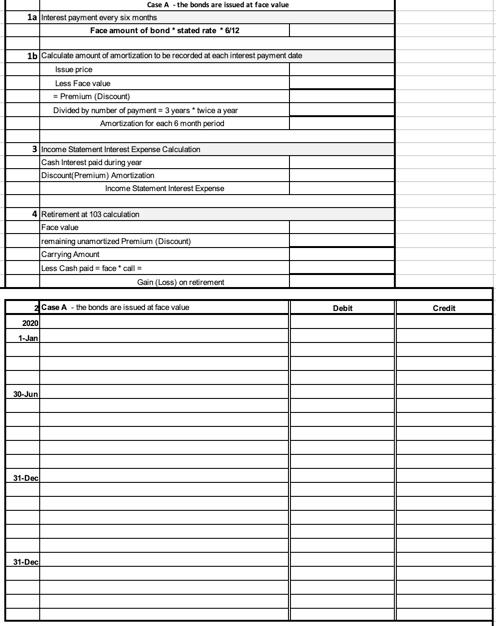

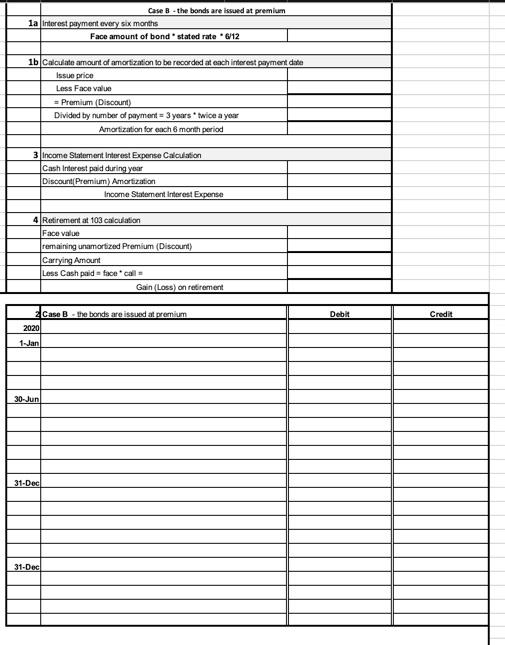

Tron Corp. was authorized to issue $500,000 of face value bonds, as follows: Date of Interest authorization Term rate Interest payment dates January 1, 2020 3 years 12% Semi-annually on June 30 and December 31 The corporation issued $250,000 of bonds on January 1, 2020 Required: Answer the questions for each of these independent cases. Case A: the bonds are issued at face value. Case B: the bonds are issued for $256,000. Case C: the bonds are issued for $242,800. 1. Calculate a. the amount of interest paid on the issued bonds every interest payment date; b. the amount of amortization, if any, applicable to each interest payment date (use the straight-line method of amortization). 2. Prepare journal entries to record a. the issue of the bonds; b. the payment of interest and recording of amortization, if any, on June 30, 2020; c. the payment of interest and recording of amortization, if any, on December 31, 2020. 3. Calculate the amount of interest expense shown in the income statement at December 31, 2020. Is this amount the same as cash paid by Tron in 2020? Why or why not? 4. On December 31, 2020, the corporation exercised a call feature included in the bond indenture and retired the $250,000 of face value bonds issued January 1, 2020. The bonds were called at 103. Prepare the December 31 journal entry to record the exercise of the call option. Assume interest and amortization journal entries have been recorded. Case A-the bonds are issued at face value la interest payment overy six months Face amount of bond stated rate 6/12 16 Calculate amount of amortization to be recorded at each interest payment date Issue price Less Face value = Premium (Discount) Divided by number of payment 3 years twice a year Amortization for each 6 month period 3 Income Statement interest Expense Calculation Cash Interest paid during year Discount(Premium) Amortization Income Statement Interest Expense 4 Retirement at 103 calculation Face value remaining un amortized Premium (Discount) Carrying Amount Less Cash paid face call Gain (Loss) on retirement Case A - the bonds are issued at face value Debit Credit 2020 30-Jun 31-Dec 31-Dec Case B - the bonds are issued at premium 1a interest payment every six months Face amount of bond stated rate "12 1b Calculate amount of amortization to be recorded at each interest payment date Issue price Less Face value = Premium Discount) Divided by number of payment 3 years twice a year Amortization for each month period 3 Income Statement Interest Expense Calculation Cash Interest paid during your Discount Premium) Amortization Income Statement interest Expense 4 Retirement at 103 calculation Face value remaining unamortized Premium (Discount) Carrying Amount Loss Cash paid focecall Gain Loss) on retirement Debit Credit 2 Case B. the bonds are issued at premium 2020 1 Jan 30-Jun 31-Dec 31-Dec Case the bonds and discount 1a interest payment every six months Face amount of bond stated rate 6/12 1. Calculate amount of amortization to be recorded at each interest payment date Issue Less Face value Premium (Discount Divided by number of payment = 3 years twice a year Amortization for each month period 3 Income Statement Interest Expense Calculation Cash Interest paid during your Discount Premium) Amortization Income Statement interest Expense 4 Retirement at 103 calculation Face value remaining unamorized Premium (Discount) Casing Amount Less Cash pada face call Gain Losson retirement Case Cthe bonds are issued at discount Credit 2020 1 Jan 30 Jun 31 Dec 31 Dec Tron Corp. was authorized to issue $500,000 of face value bonds, as follows: Date of Interest authorization Term rate Interest payment dates January 1, 2020 3 years 12% Semi-annually on June 30 and December 31 The corporation issued $250,000 of bonds on January 1, 2020 Required: Answer the questions for each of these independent cases. Case A: the bonds are issued at face value. Case B: the bonds are issued for $256,000. Case C: the bonds are issued for $242,800. 1. Calculate a. the amount of interest paid on the issued bonds every interest payment date; b. the amount of amortization, if any, applicable to each interest payment date (use the straight-line method of amortization). 2. Prepare journal entries to record a. the issue of the bonds; b. the payment of interest and recording of amortization, if any, on June 30, 2020; c. the payment of interest and recording of amortization, if any, on December 31, 2020. 3. Calculate the amount of interest expense shown in the income statement at December 31, 2020. Is this amount the same as cash paid by Tron in 2020? Why or why not? 4. On December 31, 2020, the corporation exercised a call feature included in the bond indenture and retired the $250,000 of face value bonds issued January 1, 2020. The bonds were called at 103. Prepare the December 31 journal entry to record the exercise of the call option. Assume interest and amortization journal entries have been recorded. Case A-the bonds are issued at face value la interest payment overy six months Face amount of bond stated rate 6/12 16 Calculate amount of amortization to be recorded at each interest payment date Issue price Less Face value = Premium (Discount) Divided by number of payment 3 years twice a year Amortization for each 6 month period 3 Income Statement interest Expense Calculation Cash Interest paid during year Discount(Premium) Amortization Income Statement Interest Expense 4 Retirement at 103 calculation Face value remaining un amortized Premium (Discount) Carrying Amount Less Cash paid face call Gain (Loss) on retirement Case A - the bonds are issued at face value Debit Credit 2020 30-Jun 31-Dec 31-Dec Case B - the bonds are issued at premium 1a interest payment every six months Face amount of bond stated rate "12 1b Calculate amount of amortization to be recorded at each interest payment date Issue price Less Face value = Premium Discount) Divided by number of payment 3 years twice a year Amortization for each month period 3 Income Statement Interest Expense Calculation Cash Interest paid during your Discount Premium) Amortization Income Statement interest Expense 4 Retirement at 103 calculation Face value remaining unamortized Premium (Discount) Carrying Amount Loss Cash paid focecall Gain Loss) on retirement Debit Credit 2 Case B. the bonds are issued at premium 2020 1 Jan 30-Jun 31-Dec 31-Dec Case the bonds and discount 1a interest payment every six months Face amount of bond stated rate 6/12 1. Calculate amount of amortization to be recorded at each interest payment date Issue Less Face value Premium (Discount Divided by number of payment = 3 years twice a year Amortization for each month period 3 Income Statement Interest Expense Calculation Cash Interest paid during your Discount Premium) Amortization Income Statement interest Expense 4 Retirement at 103 calculation Face value remaining unamorized Premium (Discount) Casing Amount Less Cash pada face call Gain Losson retirement Case Cthe bonds are issued at discount Credit 2020 1 Jan 30 Jun 31 Dec 31 Dec

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts