Question: Please include R code A stochastic process is a (potentially innite) collection of random variables Xt where the index i: is usually thought of as

Please include R code

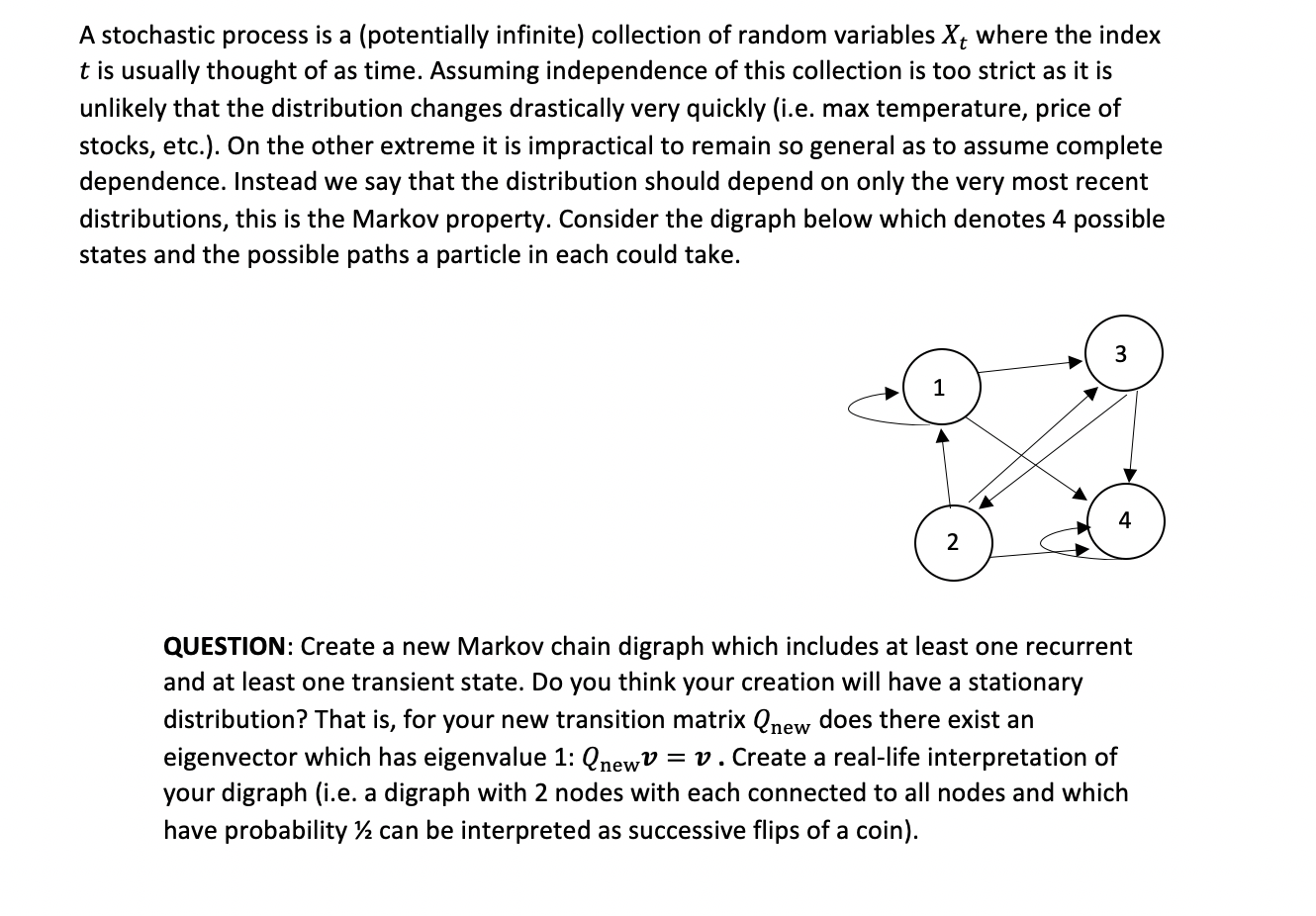

A stochastic process is a (potentially innite) collection of random variables Xt where the index i: is usually thought of as time. Assuming independence of this collection is too strict as it is unlikely that the distribution changes drastically very quickly (i.e. max temperature, price of stocks, etc.). On the other extreme it is impractical to remain so general as to assume complete dependence. Instead we say that the distribution should depend on only the very most recent distributions, this is the Markov property. Consider the digraph below which denotes 4 possible states and the possible paths a particle in each could take. 04x0 QUESTION: Create a new Markov chain digraph which includes at least one recurrent and at least one transient state. Do you think your creation will have a stationary distribution? That is, for your new transition matrix Qnew does there exist an eigenvector which has eigenvalue 1: Qnewv = v . Create a real-life interpretation of your digraph (Le. a digraph with 2 nodes with each connected to all nodes and which have probability 16 can be interpreted as successive flips of a coin}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts