Question: please only answer if you know how to solve for it. this is my 3rd attempt to get help on this question Question 3 0/1

please only answer if you know how to solve for it. this is my 3rd attempt to get help on this question

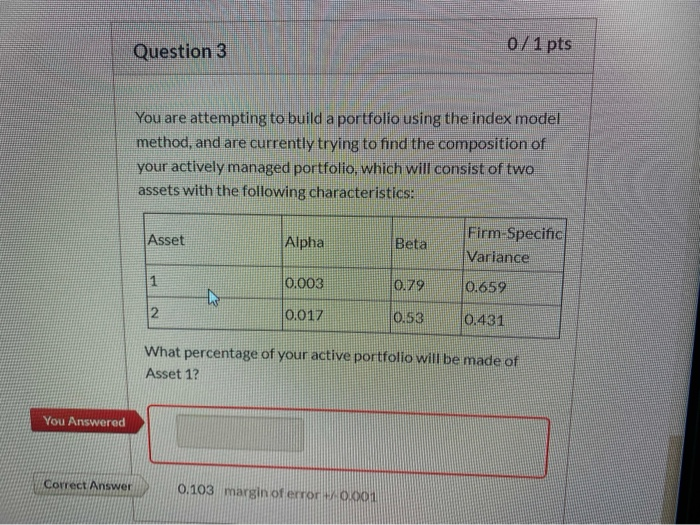

Question 3 0/1 pts You are attempting to build a portfolio using the index model method, and are currently trying to find the composition of your actively managed portfolio, which will consist of two assets with the following characteristics: Asset Alpha Beta Firm-Specific Variance 0.79 0.659 0.003 0.017 0.53 0.431 What percentage of your active portfolio will be made of Asset 12 You Answered Correct Answer 0.103 margin of error 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock