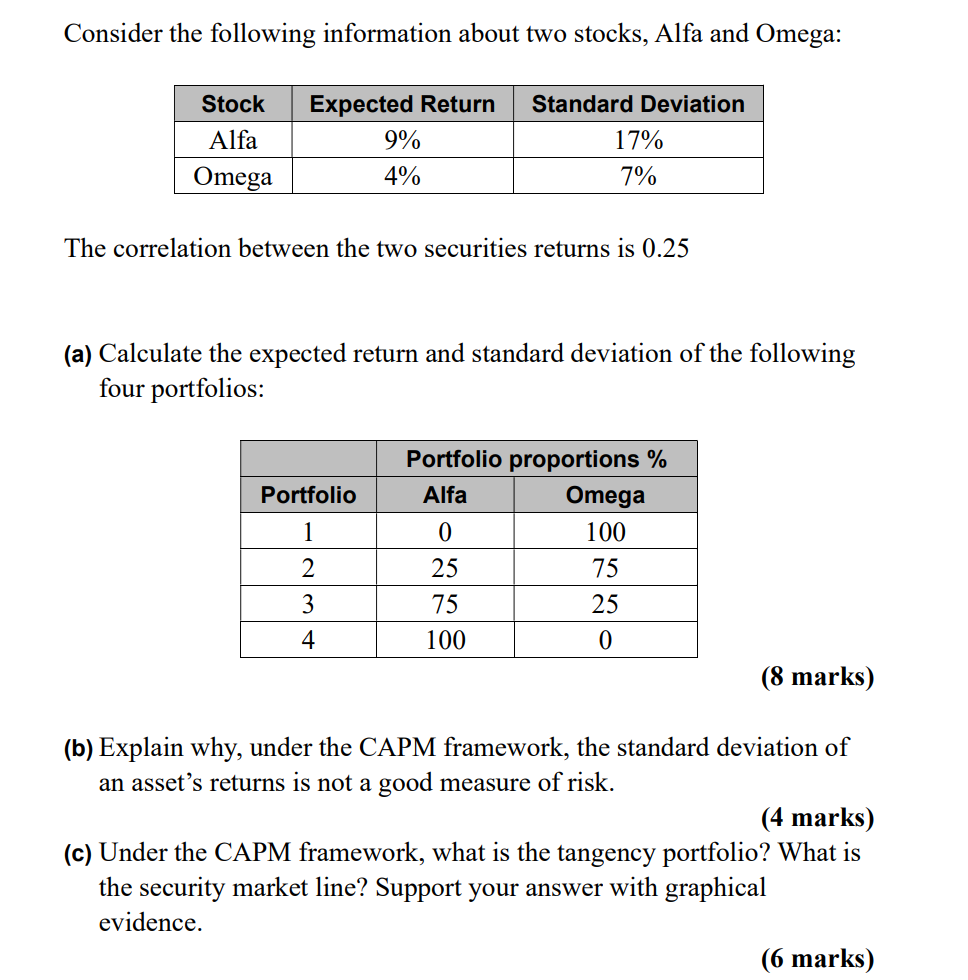

Question: Please only answer the question (c) Consider the following information about two stocks, Alfa and Omega: Alfa 9% 17% Omega 4% 7% The correlation between

Please only answer the question (c)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock