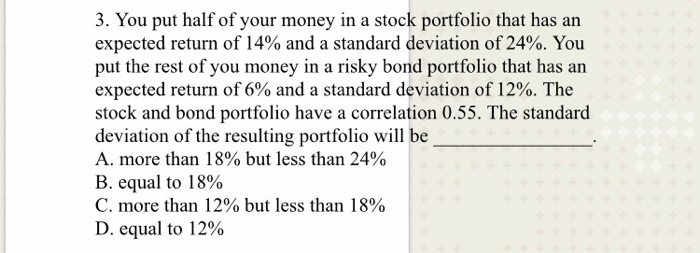

Question: please provide a breakdown along with equations. 3. You put half of your money in a stock portfolio that has an expected return of 14%

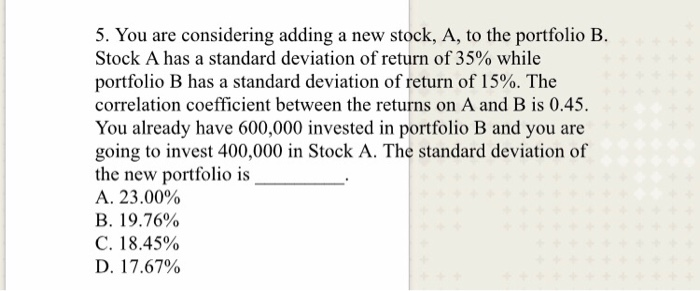

3. You put half of your money in a stock portfolio that has an expected return of 14% and a standard deviation of 24%. You put the rest of you money in a risky bond portfolio that has an expected return of 6% and a standard deviation of 12%. The stock and bond portfolio have a correlation 0.55. The standard deviation of the resulting portfolio will be A. more than 18% but less than 24% B. equal to 18% C. more than 12% but less than 18% D. equal to 12% 5. You are considering adding a new stock, A, to the portfolio B. Stock A has a standard deviation of return of 35% while portfolio B has a standard deviation of return of 15%. The correlation coefficient between the returns on A and B is 0.45. You already have 600,000 invested in portfolio B and you are going to invest 400,000 in Stock A. The standard deviation of the new portfolio is A. 23.00% . 19.76% C. 18.45% D. 17.67%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts