Question: Please provide complete calculations, explanations and proofs. 2. Portfolio hedging. An important role of a portfolio manager is to control for risk. For example, a

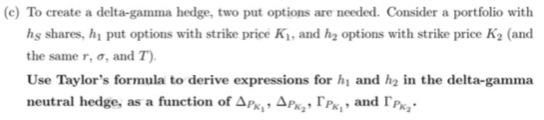

2. Portfolio hedging. An important role of a portfolio manager is to control for risk. For example, a portfolio may contain a high number of shares in an individual firm and therefore be highly exposed to movements of the stock price, S, of that firm. One way of hedging the risk of S changing is, of course, to sell some of the shares, but for various reasons this may not be feasible. Another approach is then to purchase another asset that increases in value if the stock price decreases. Mathematically, if the price of this hedging asset is P. this is expressed by requiring that 0 We define the number Ap = , which is denoted by the "delta" of the hedging asset (with respect to stock price risk). A delta hedge is implemented by purchasing an amount of the hedging asset such that the portfolio is neutral to small movements of the stock price, i.e., such that hs + hpAp=0. We arrive at hs. hp = for the delta hedge, where positivity follows from the assumption that Ap 0. We define the number Ap = *, which is denoted by the "delta of the hedging asset (with respect to stock price risk). A delta hedge is implemented by purchasing an amount of the hedging asset such that the portfolio is neutral to small movements of the stock price, i.e., such that hs +hpAp=0We arrive at hp hy > AP for the delta hedge, where positivity follows from the assumption that Ap 0 We define the number Ap = , which is denoted by the "delta" of the hedging asset (with respect to stock price risk). A delta hedge is implemented by purchasing an amount of the hedging asset such that the portfolio is neutral to small movements of the stock price, i.e., such that hs + hpAp=0. We arrive at hs. hp = for the delta hedge, where positivity follows from the assumption that Ap 0. We define the number Ap = *, which is denoted by the "delta of the hedging asset (with respect to stock price risk). A delta hedge is implemented by purchasing an amount of the hedging asset such that the portfolio is neutral to small movements of the stock price, i.e., such that hs +hpAp=0We arrive at hp hy > AP for the delta hedge, where positivity follows from the assumption that Ap

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts