Question: Please provide correct solutions with step-by-step workings/explanations. Based on the AIC criteria, we select the ARMA(2,0) model using the detrended time series. The second order

Please provide correct solutions with step-by-step workings/explanations.

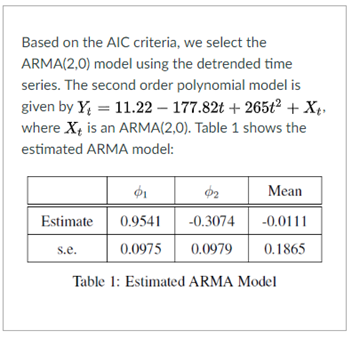

Based on the AIC criteria, we select the ARMA(2,0) model using the detrended time series. The second order polynomial model is given by Y = 11.22 - 177.82t + 265t' + Xt. where X, is an ARMA(2,0). Table 1 shows the estimated ARMA model: Mean Estimate 0.9541 -0.3074 -0.0111 s.e. 0.0975 0.0979 0.1865 Table 1: Estimated ARMA ModelCross-covariances are symmetric in k : cov (yit, yit-k ) = cov (yit, yittk ) when i = j

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock