Question: Please provide explanation for both questions. 2. Consider a standard portfolio choice problem with two risky assets: equity and risky bond. Their expected returns, standard

Please provide explanation for both questions.

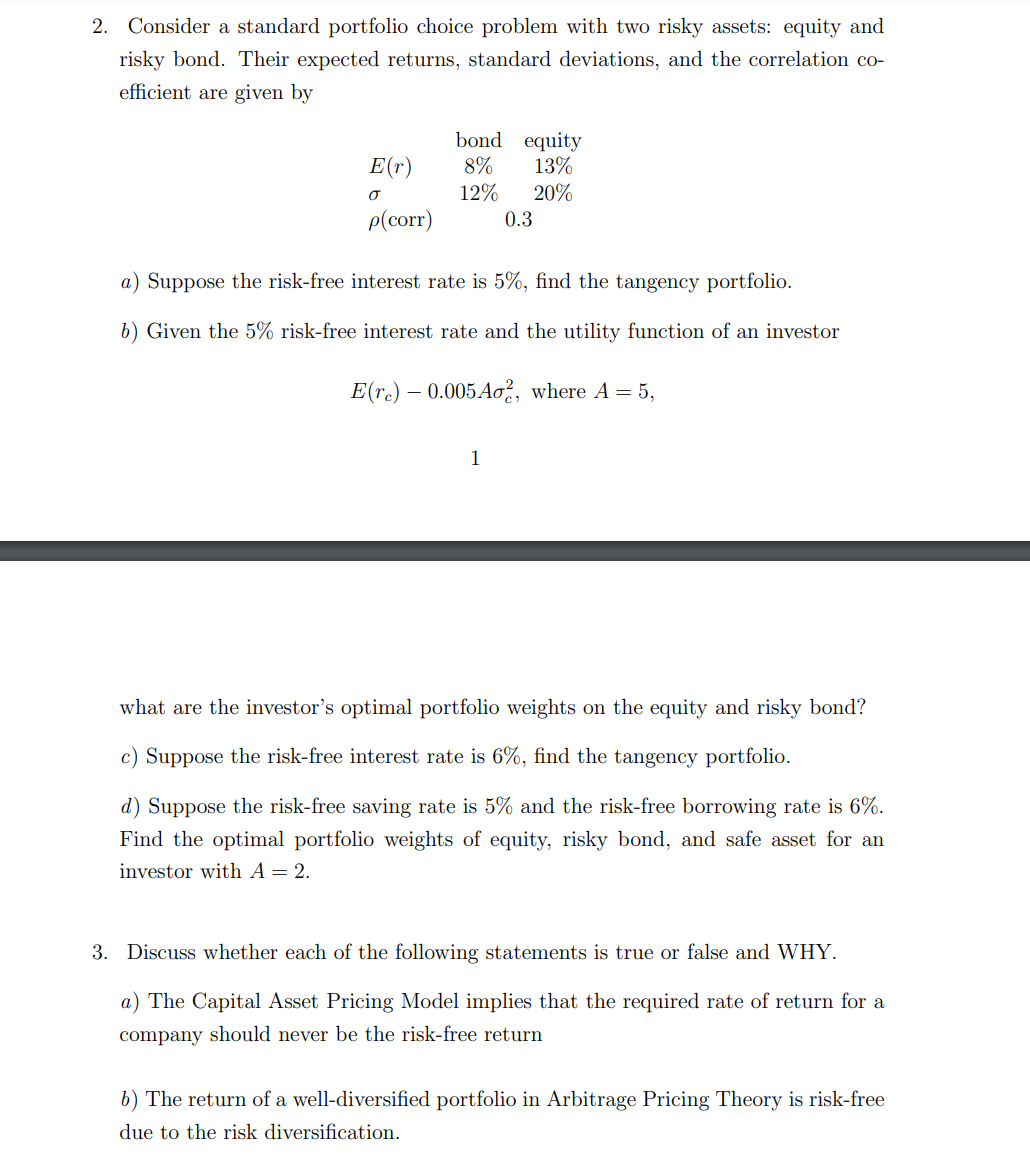

2. Consider a standard portfolio choice problem with two risky assets: equity and risky bond. Their expected returns, standard deviations, and the correlation coefficient are given by a) Suppose the risk-free interest rate is 5%, find the tangency portfolio. b) Given the 5% risk-free interest rate and the utility function of an investor E(rc)0.005Ac2,whereA=5, 1 what are the investor's optimal portfolio weights on the equity and risky bond? c) Suppose the risk-free interest rate is 6%, find the tangency portfolio. d) Suppose the risk-free saving rate is 5% and the risk-free borrowing rate is 6%. Find the optimal portfolio weights of equity, risky bond, and safe asset for an investor with A=2. 3. Discuss whether each of the following statements is true or false and WHY. a) The Capital Asset Pricing Model implies that the required rate of return for a company should never be the risk-free return b) The return of a well-diversified portfolio in Arbitrage Pricing Theory is risk-free due to the risk diversification

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts