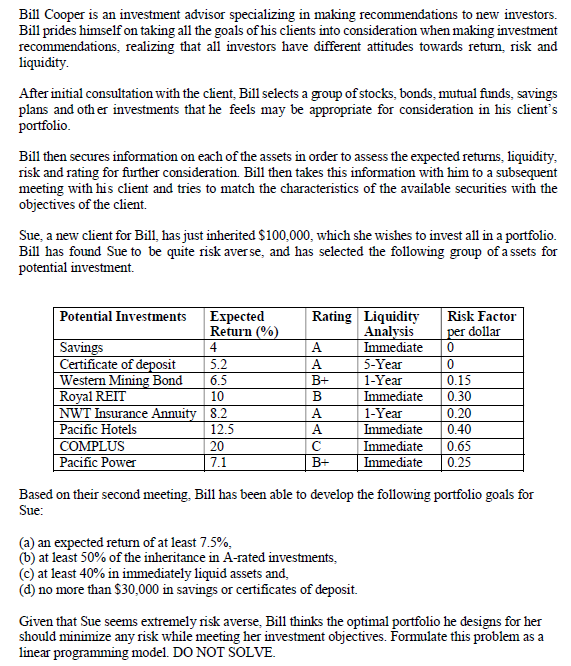

Question: Please provide the decision variables, objective function, and constraints. Ideally on paper and not excel. Bill Cooper is an investment advisor specializing in making recommendations

Please provide the decision variables, objective function, and constraints. Ideally on paper and not excel.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock