Question: PLEASE READ MY ACTUAL QUESTION AND DO NOT COPY PASTE ANSWERS FROM OTHER CHEGG PROBLEMS PLEASE THIS IS MY THIRD TIME TRYING TO GET A

PLEASE READ MY ACTUAL QUESTION AND DO NOT COPY PASTE ANSWERS FROM OTHER CHEGG PROBLEMS PLEASE

THIS IS MY THIRD TIME TRYING TO GET A REAL RESPONSE FROM A CHEGG USER INSTEAD OF COPYING AND PASTING THE SAME ANSWER FROM ANOTHER QUESTION

QUESTION IN REGARDS TO THE SECOND PHOTO OF ROSA CORPORATION: How control is defined and how we know whether both of these transactions meet that definition.

PLEASE DO NOT ANSWER WITH THE FOLLOWING RESPONSE (picture below): I AM ASKING A COMPLETELY SEPARATE QUESTION

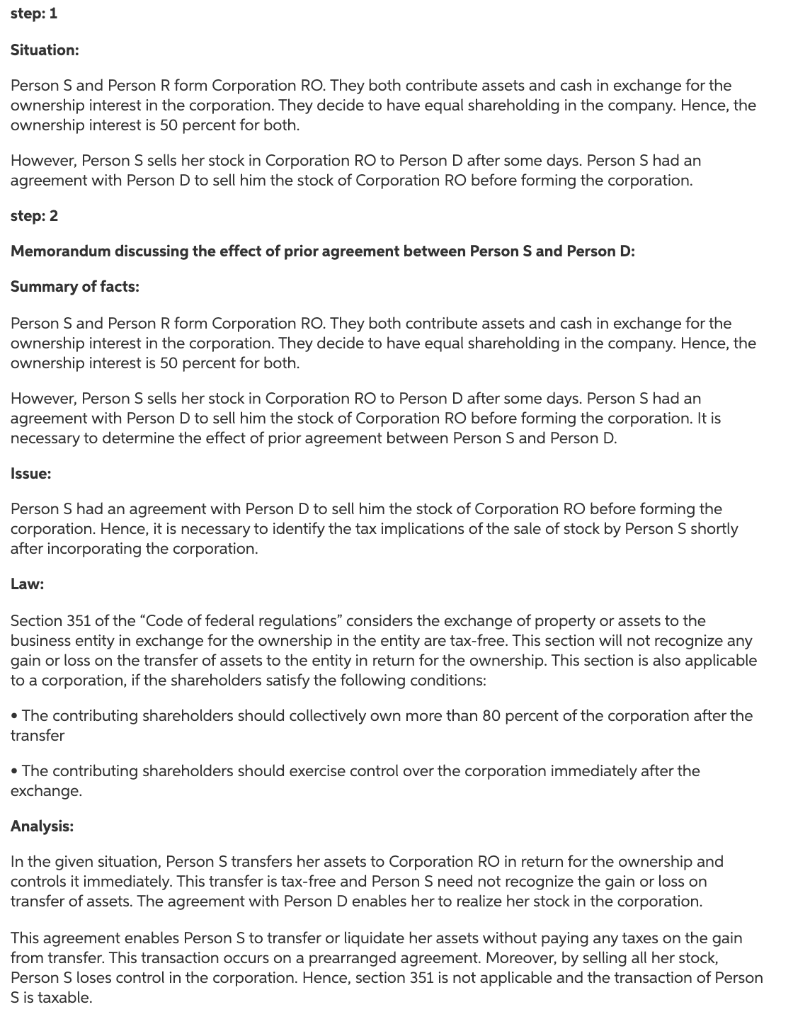

step: 1 Situation: Person S and Person R form Corporation RO. They both contribute assets and cash in exchange for the ownership interest in the corporation. They decide to have equal shareholding in the company. Hence, the ownership interest is 50 percent for both. However, Person S sells her stock in Corporation RO to Person D after some days. Person Shad an agreement with Person D to sell him the stock of Corporation RO before forming the corporation. step: 2 Memorandum discussing the effect of prior agreement between Person S and Person D: Summary of facts: Person S and Person R form Corporation RO. They both contribute assets and cash in exchange for the ownership interest in the corporation. They decide to have equal shareholding in the company. Hence, the ownership interest is 50 percent for both. However, Person S sells her stock in Corporation RO to Person D after some days. Person Shad an agreement with Person D to sell him the stock of Corporation RO before forming the corporation. It is necessary to determine the effect of prior agreement between Person S and Person D. Issue: Person Shad an agreement with Person D to sell him the stock of Corporation RO before forming the corporation. Hence, it is necessary to identify the tax implications of the sale of stock by Person S shortly after incorporating the corporation. Law: Section 351 of the "Code of federal regulations" considers the exchange of property or assets to the business entity in exchange for the ownership in the entity are tax-free. This section will not recognize any gain or loss on the transfer of assets to the entity in return for the ownership. This section is also applicable to a corporation, if the shareholders satisfy the following conditions: The contributing shareholders should collectively own more than 80 percent of the corporation after the transfer The contributing shareholders should exercise control over the corporation immediately after the exchange. Analysis: In the given situation, Person Stransfers her assets to Corporation RO in return for the ownership and controls it immediately. This transfer is tax-free and Person S need not recognize the gain or loss on transfer of assets. The agreement with Person D enables her to realize her stock in the corporation. This agreement enables Person S to transfer or liquidate her assets without paying any taxes on the gain from transfer. This transaction occurs on a prearranged agreement. Moreover, by selling all her stock, Person Sloses control in the corporation. Hence, section 351 is not applicable and the transaction of Person S is taxable. Shirley and Roseann form Rosa Corporation with each contributing assets and cash in exchange for all of the corporation's stock. Shirley and Roseann each own 50 percent of the stock immediately after the exchange. Shortly thereafter, Shirley sells all her stock to Don per a written agreement executed before the formation of Rosa Corporation. Prepare a memorandum discussing the effect of this prearranged agreement. step: 1 Situation: Person S and Person R form Corporation RO. They both contribute assets and cash in exchange for the ownership interest in the corporation. They decide to have equal shareholding in the company. Hence, the ownership interest is 50 percent for both. However, Person S sells her stock in Corporation RO to Person D after some days. Person Shad an agreement with Person D to sell him the stock of Corporation RO before forming the corporation. step: 2 Memorandum discussing the effect of prior agreement between Person S and Person D: Summary of facts: Person S and Person R form Corporation RO. They both contribute assets and cash in exchange for the ownership interest in the corporation. They decide to have equal shareholding in the company. Hence, the ownership interest is 50 percent for both. However, Person S sells her stock in Corporation RO to Person D after some days. Person Shad an agreement with Person D to sell him the stock of Corporation RO before forming the corporation. It is necessary to determine the effect of prior agreement between Person S and Person D. Issue: Person Shad an agreement with Person D to sell him the stock of Corporation RO before forming the corporation. Hence, it is necessary to identify the tax implications of the sale of stock by Person S shortly after incorporating the corporation. Law: Section 351 of the "Code of federal regulations" considers the exchange of property or assets to the business entity in exchange for the ownership in the entity are tax-free. This section will not recognize any gain or loss on the transfer of assets to the entity in return for the ownership. This section is also applicable to a corporation, if the shareholders satisfy the following conditions: The contributing shareholders should collectively own more than 80 percent of the corporation after the transfer The contributing shareholders should exercise control over the corporation immediately after the exchange. Analysis: In the given situation, Person Stransfers her assets to Corporation RO in return for the ownership and controls it immediately. This transfer is tax-free and Person S need not recognize the gain or loss on transfer of assets. The agreement with Person D enables her to realize her stock in the corporation. This agreement enables Person S to transfer or liquidate her assets without paying any taxes on the gain from transfer. This transaction occurs on a prearranged agreement. Moreover, by selling all her stock, Person Sloses control in the corporation. Hence, section 351 is not applicable and the transaction of Person S is taxable. Shirley and Roseann form Rosa Corporation with each contributing assets and cash in exchange for all of the corporation's stock. Shirley and Roseann each own 50 percent of the stock immediately after the exchange. Shortly thereafter, Shirley sells all her stock to Don per a written agreement executed before the formation of Rosa Corporation. Prepare a memorandum discussing the effect of this prearranged agreement

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts