Question: please reply as a screenshot of excel and function~ also need to explain ~ thanks Question 1: Delta and Gamma Hedging Strategy (18 Marks] The

please reply as a screenshot of excel and function~ also need to explain ~ thanks

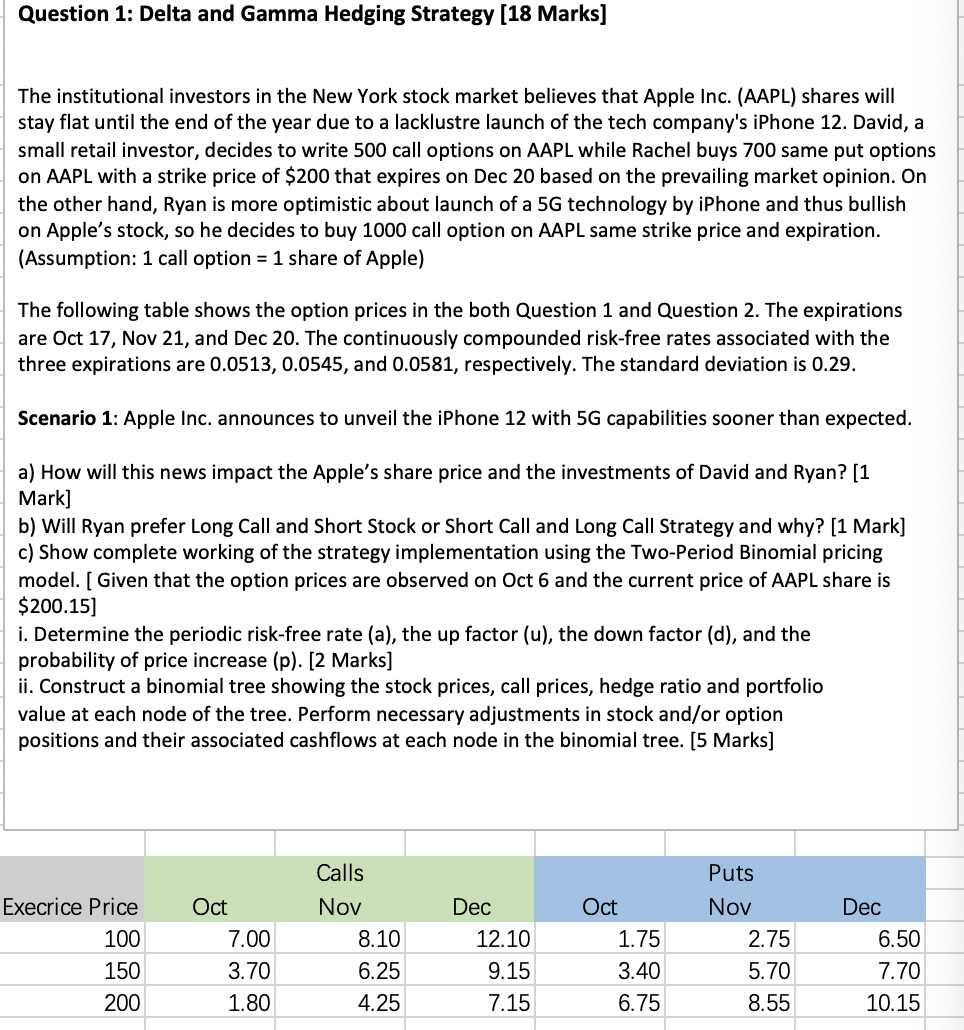

Question 1: Delta and Gamma Hedging Strategy (18 Marks] The institutional investors in the New York stock market believes that Apple Inc. (AAPL) shares will stay flat until the end of the year due to a lacklustre launch of the tech company's iPhone 12. David, a small retail investor, decides to write 500 call options on AAPL while Rachel buys 700 same put options on AAPL with a strike price of $200 that expires on Dec 20 based on the prevailing market opinion. On the other hand, Ryan is more optimistic about launch of a 5G technology by iPhone and thus bullish on Apple's stock, so he decides to buy 1000 call option on AAPL same strike price and expiration. (Assumption: 1 call option = 1 share of Apple) The following table shows the option prices in the both Question 1 and Question 2. The expirations are Oct 17, Nov 21, and Dec 20. The continuously compounded risk-free rates associated with the three expirations are 0.0513, 0.0545, and 0.0581, respectively. The standard deviation is 0.29. Scenario 1: Apple Inc. announces to unveil the iPhone 12 with 5G capabilities sooner than expected. a) How will this news impact the Apple's share price and the investments of David and Ryan? [1 Mark] b) Will Ryan prefer Long Call and Short Stock or Short Call and Long Call Strategy and why? [1 Mark] c) Show complete working of the strategy implementation using the Two-Period Binomial pricing model. [ Given that the option prices are observed on Oct 6 and the current price of AAPL share is $200.15] i. Determine the periodic risk-free rate (a), the up factor (u), the down factor (d), and the probability of price increase (p). [2 marks] ii. Construct a binomial tree showing the stock prices, call prices, hedge ratio and portfolio value at each node of the tree. Perform necessary adjustments in stock and/or option positions and their associated cashflows at each node in the binomial tree. (5 Marks] Puts Execrice Price 100 150 200 Oct 7.00 3.70 1.80 Calls Nov 8.10 6.25 4.25 Dec 12.10 9.15 7.15 Oct 1.75 3.40 6.75 Nov 2.75 5.70 8.55 Dec 6.50 7.70 10.15 Question 1: Delta and Gamma Hedging Strategy (18 Marks] The institutional investors in the New York stock market believes that Apple Inc. (AAPL) shares will stay flat until the end of the year due to a lacklustre launch of the tech company's iPhone 12. David, a small retail investor, decides to write 500 call options on AAPL while Rachel buys 700 same put options on AAPL with a strike price of $200 that expires on Dec 20 based on the prevailing market opinion. On the other hand, Ryan is more optimistic about launch of a 5G technology by iPhone and thus bullish on Apple's stock, so he decides to buy 1000 call option on AAPL same strike price and expiration. (Assumption: 1 call option = 1 share of Apple) The following table shows the option prices in the both Question 1 and Question 2. The expirations are Oct 17, Nov 21, and Dec 20. The continuously compounded risk-free rates associated with the three expirations are 0.0513, 0.0545, and 0.0581, respectively. The standard deviation is 0.29. Scenario 1: Apple Inc. announces to unveil the iPhone 12 with 5G capabilities sooner than expected. a) How will this news impact the Apple's share price and the investments of David and Ryan? [1 Mark] b) Will Ryan prefer Long Call and Short Stock or Short Call and Long Call Strategy and why? [1 Mark] c) Show complete working of the strategy implementation using the Two-Period Binomial pricing model. [ Given that the option prices are observed on Oct 6 and the current price of AAPL share is $200.15] i. Determine the periodic risk-free rate (a), the up factor (u), the down factor (d), and the probability of price increase (p). [2 marks] ii. Construct a binomial tree showing the stock prices, call prices, hedge ratio and portfolio value at each node of the tree. Perform necessary adjustments in stock and/or option positions and their associated cashflows at each node in the binomial tree. (5 Marks] Puts Execrice Price 100 150 200 Oct 7.00 3.70 1.80 Calls Nov 8.10 6.25 4.25 Dec 12.10 9.15 7.15 Oct 1.75 3.40 6.75 Nov 2.75 5.70 8.55 Dec 6.50 7.70 10.15

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts