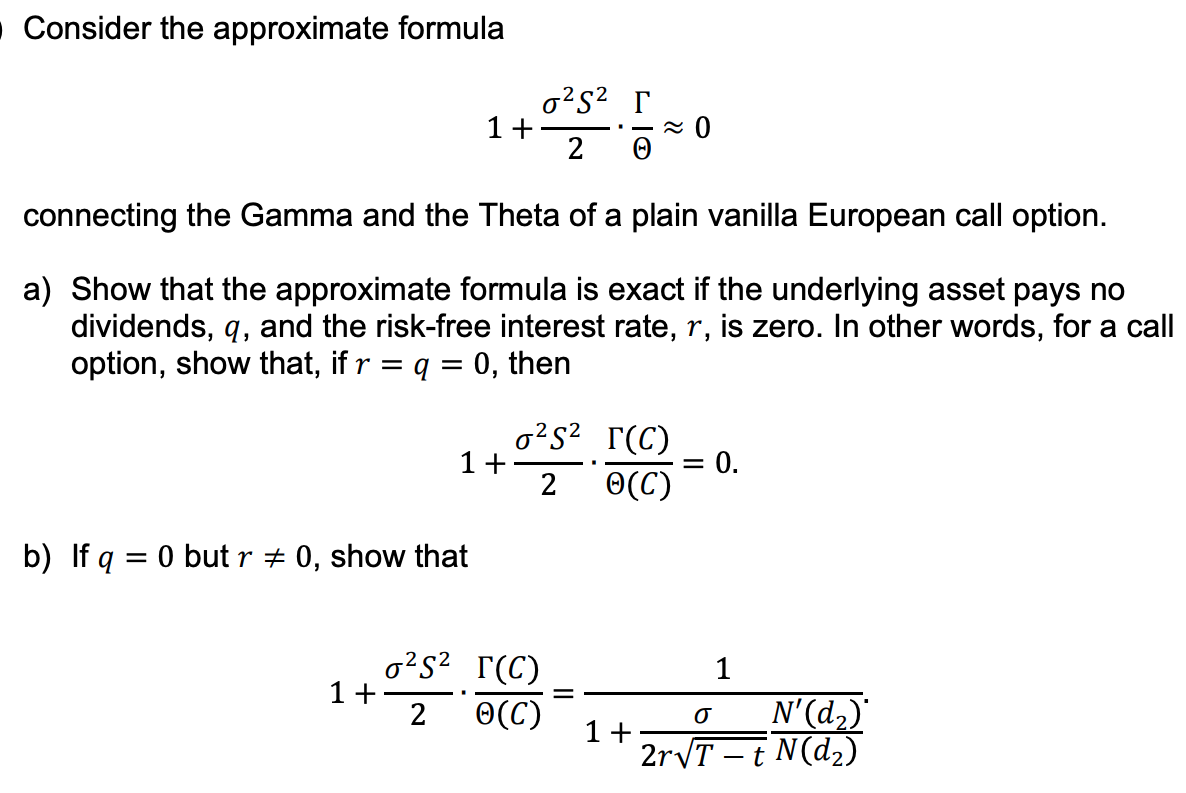

Question: Please see the attachment Consider the approximate formula 1 + ~ 0 2 connecting the Gamma and the Theta of a plain vanilla European call

Please see the attachment

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock