Question: please show all the work manually. not using excel for any of the answers. please specify which part you are answering. thank you ! 18.

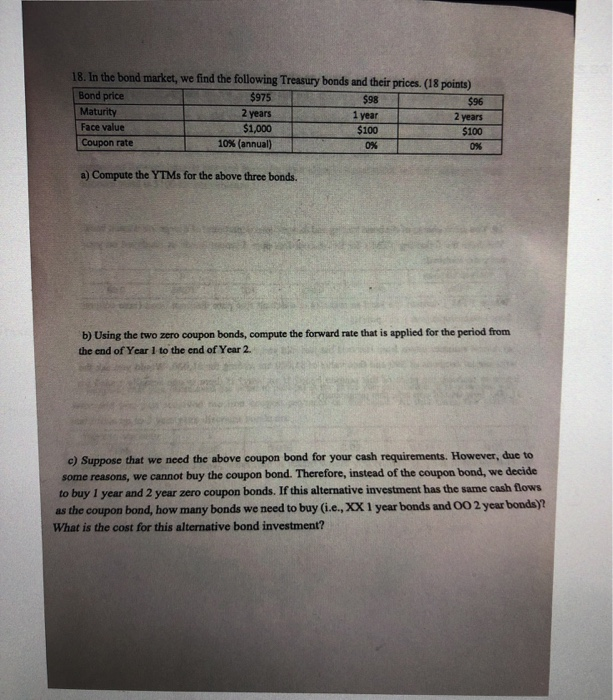

18. In the bond market, we find the following Treasury bonds and their prices. (18 points) Bond price $975 $98 $96 Maturity 2 years 1 year 2 years Face value $1,000 $100 $100 Coupon rate 10% (annual) ON a) Compute the YTMs for the above three bonds. . b) Using the two zero coupon bonds, compute the forward rate that is applied for the period from the end of Year 1 to the end of Year 2 c) Suppose that we need the above coupon bond for your cash requirements. However, due to some reasons, we cannot buy the coupon bond. Therefore, instead of the coupon bond, we decide to buy 1 year and 2 year zero coupon bonds. If this alternative investment has the same cash flows as the coupon bond, how many bonds we need to buy i.e., XX 1 year bonds and CO 2 year bonds)? What is the cost for this alternative bond investment? d) Using your work in question c), is there an arbitrage opportunity? If any, how can we transact for arbitrage? Compute the arbitrage profits. (for this question, we can assume that we can transact the coupon bond.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts