Question: please show all workings and non excel version Question 2 (12 marks) You estimated the single index (market) model for stocks A and B with

please show all workings and non excel version

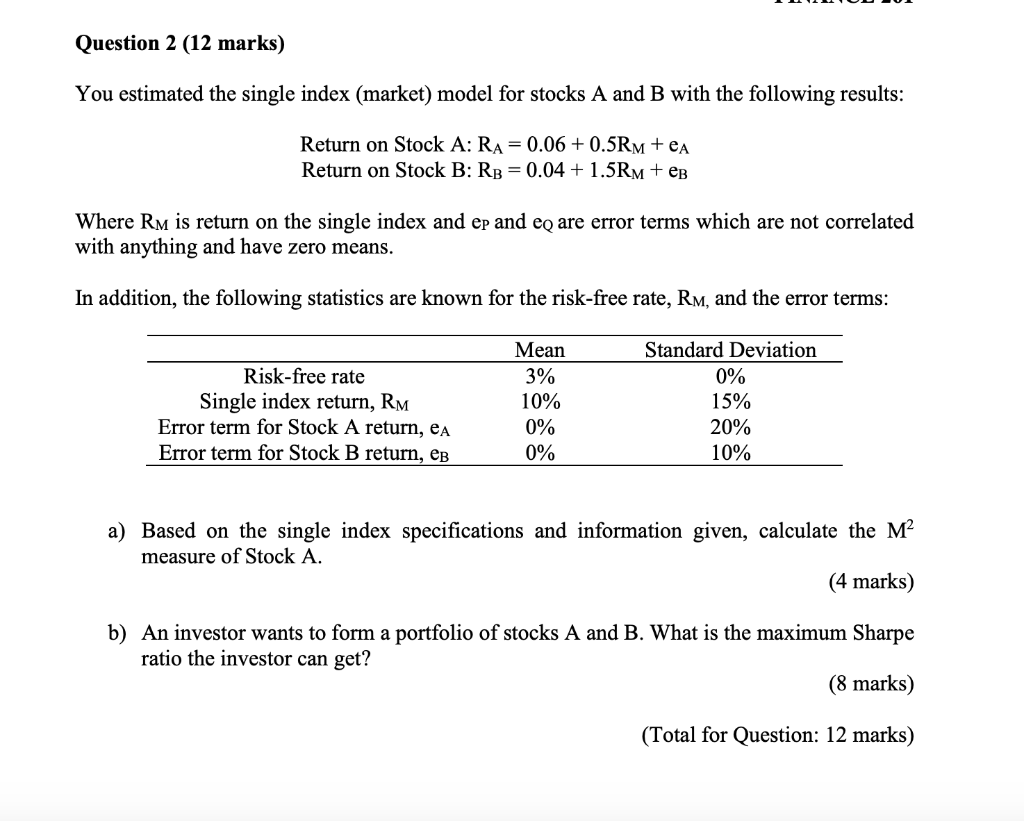

Question 2 (12 marks) You estimated the single index (market) model for stocks A and B with the following results: Return on Stock A: RA= 0.06 + 0.5RM +eA Return on Stock B: RB = 0.04 + 1.5RM + eB Where Rm is return on the single index and ep and eq are error terms which are not correlated with anything and have zero means. In addition, the following statistics are known for the risk-free rate, Rm, and the error terms: Risk-free rate Single index return, RM Error term for Stock A return, ea Error term for Stock B return, eB Mean 3% 10% 0% 0% Standard Deviation 0% 15% 20% 10% a) Based on the single index specifications and information given, calculate the M measure of Stock A. (4 marks) b) An investor wants to form a portfolio of stocks A and B. What is the maximum Sharpe ratio the investor can get? (8 marks) (Total for Question: 12 marks) Question 2 (12 marks) You estimated the single index (market) model for stocks A and B with the following results: Return on Stock A: RA= 0.06 + 0.5RM +eA Return on Stock B: RB = 0.04 + 1.5RM + eB Where Rm is return on the single index and ep and eq are error terms which are not correlated with anything and have zero means. In addition, the following statistics are known for the risk-free rate, Rm, and the error terms: Risk-free rate Single index return, RM Error term for Stock A return, ea Error term for Stock B return, eB Mean 3% 10% 0% 0% Standard Deviation 0% 15% 20% 10% a) Based on the single index specifications and information given, calculate the M measure of Stock A. (4 marks) b) An investor wants to form a portfolio of stocks A and B. What is the maximum Sharpe ratio the investor can get? (8 marks) (Total for Question: 12 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts