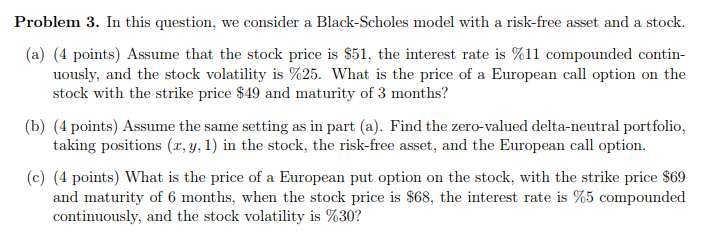

Question: Please show all work/steps. Please do not use excel or other programs. Thanks Problem 3. In this question, we consider a Black-Scholes model with a

Please show all work/steps. Please do not use excel or other programs. Thanks

Problem 3. In this question, we consider a Black-Scholes model with a risk-free asset and a stock (a) (4 points) Assume that the stock price is $51, the interest rate is %11 compounded contin- uously, and the stock volatility is %25. What is the price of a European call option on the b) (4 points) Assume the same setting as in part (a). Find the zero-valued delta-neutral portfolio, (c) (4 points) What is the price of a European put option on the stock, with the strike price $69 stock with the strike price $49 and maturity of 3 months? taking positions (x, y, 1) in the stock, the risk-free asset, and the European call option. and maturity of 6 months, when the stock price is $68, the interest rate is %5 compounded Problem 3. In this question, we consider a Black-Scholes model with a risk-free asset and a stock (a) (4 points) Assume that the stock price is $51, the interest rate is %11 compounded contin- uously, and the stock volatility is %25. What is the price of a European call option on the b) (4 points) Assume the same setting as in part (a). Find the zero-valued delta-neutral portfolio, (c) (4 points) What is the price of a European put option on the stock, with the strike price $69 stock with the strike price $49 and maturity of 3 months? taking positions (x, y, 1) in the stock, the risk-free asset, and the European call option. and maturity of 6 months, when the stock price is $68, the interest rate is %5 compounded

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts