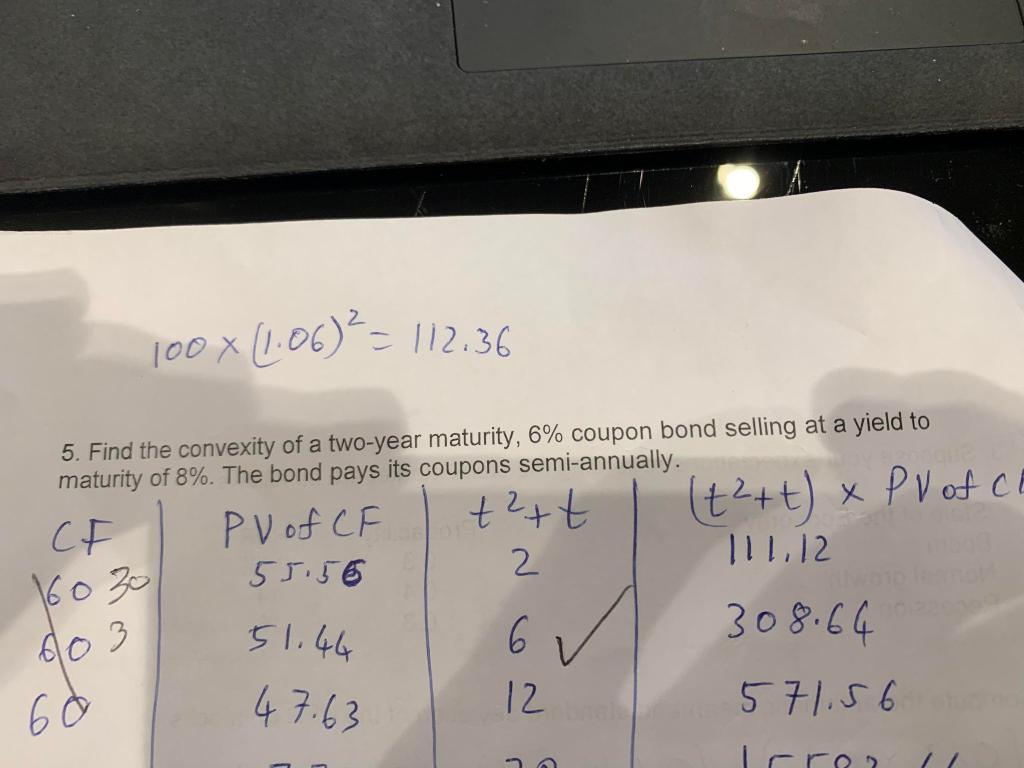

Question: Please show calculation (not Excel) 100 x (1.06)2 = 112.36 (++t) x PV of ce 5. Find the convexity of a two-year maturity, 6% coupon

Please show calculation (not Excel)

100 x (1.06)2 = 112.36 (++t) x PV of ce 5. Find the convexity of a two-year maturity, 6% coupon bond selling at a yield to maturity of 8%. The bond pays its coupons semi-annually. t2t PV of CF CF 2 11.12 55.56 6 308.64 16030 603 51.44 47.63 12 60 571.56 Irror 3 77

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock