Question: Please show clear handwriting solution. Thank you. 4. The variance covariance matrix of returns to a portfolio of three assets A,B, and C is given

Please show clear handwriting solution. Thank you.

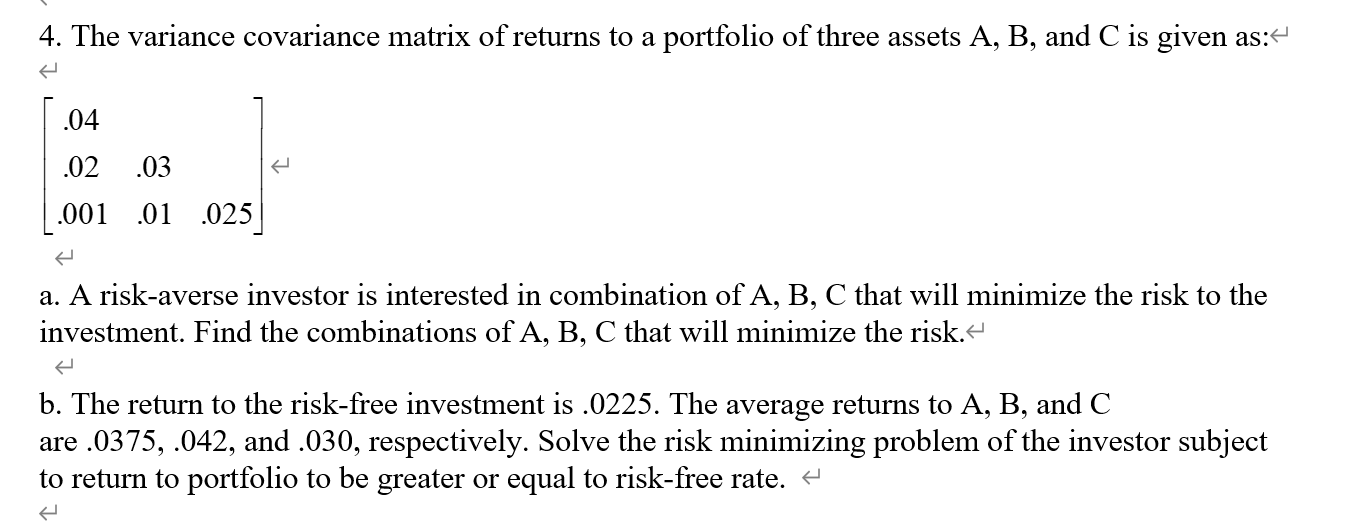

4. The variance covariance matrix of returns to a portfolio of three assets A,B, and C is given as: .04.02.001.03.01.025 a. A risk-averse investor is interested in combination of A,B,C that will minimize the risk to the investment. Find the combinations of A,B,C that will minimize the risk. b. The return to the risk-free investment is .0225 . The average returns to A,B, and C are .0375,.042, and .030 , respectively. Solve the risk minimizing problem of the investor subject to return to portfolio to be greater or equal to risk-free rate

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock