Question: PLEASE show coding used. Suppose you are given the information about the default-free, coupon-paying yield curve below. a. Use arbitrage to determine the yield to

PLEASE show coding used.

PLEASE show coding used.

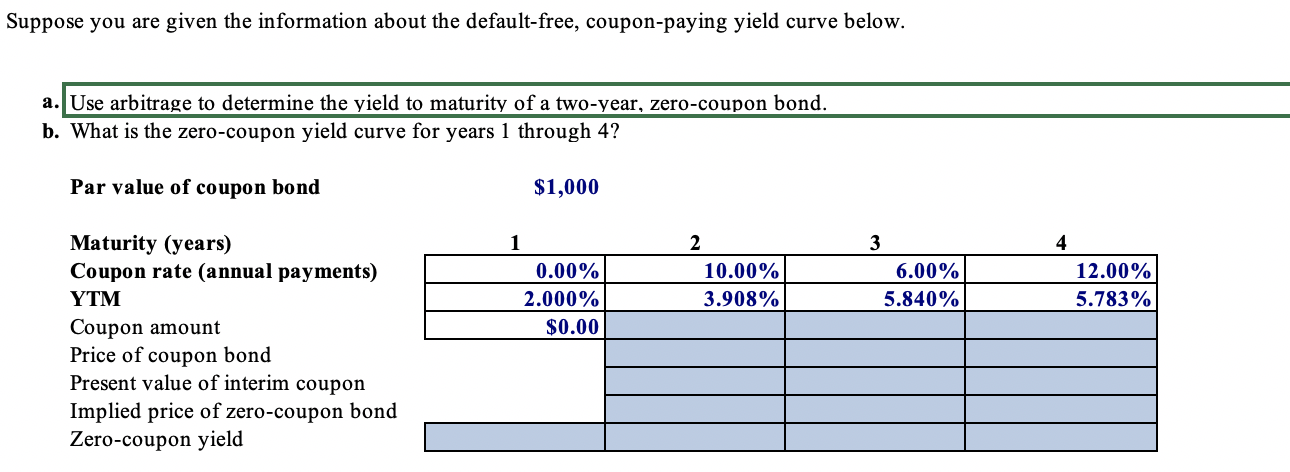

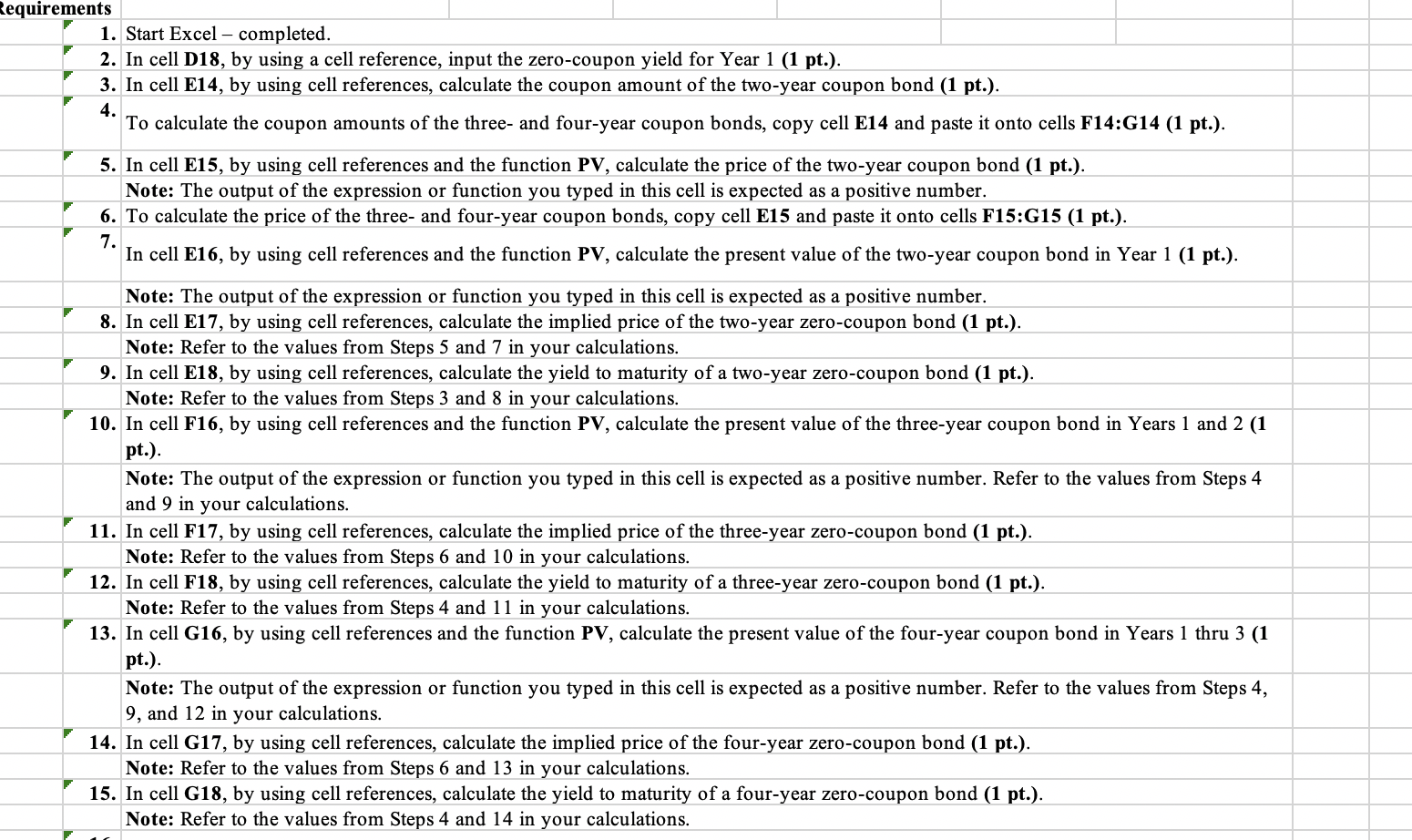

Suppose you are given the information about the default-free, coupon-paying yield curve below. a. Use arbitrage to determine the yield to maturity of a two-year, zero-coupon bond. b. What is the zero-coupon yield curve for years 1 through 4? Par value of coupon bond $1,000 1 0.00% 2.000% $0.00 2 10.00% 3.908% 3 6.00% 5.840% 4 12.00% 5.783% Maturity (years) Coupon rate (annual payments) YTM Coupon amount Price of coupon bond Present value of interim coupon Implied price of zero-coupon bond Zero-coupon yield Requirements 1. Start Excel - completed. 2. In cell D18, by using a cell reference, input the zero-coupon yield for Year 1 (1 pt.). 3. In cell E14, by using cell references, calculate the coupon amount of the two-year coupon bond (1 pt.). 4. To calculate the coupon amounts of the three- and four-year coupon bonds, copy cell E14 and paste it onto cells F14:G14 (1 pt.). 5. In cell E15, by using cell references and the function PV, calculate the price of the two-year coupon bond (1 pt.). Note: The output of the expression or function you typed in this cell is expected as a positive number. 6. To calculate the price of the three- and four-year coupon bonds, copy cell E15 and paste it onto cells F15:G15 (1 pt.). 7. In cell E16, by using cell references and the function PV, calculate the present value of the two-year coupon bond in Year 1 (1 pt.). Note: The output of the expression or function you typed in this cell is expected as a positive number. 8. In cell E17, by using cell references, calculate the implied price of the two-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 5 and 7 in your calculations. 9. In cell E18, by using cell references, calculate the yield to maturity of a two-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 3 and 8 in your calculations. 10. In cell F16, by using cell references and the function PV, calculate the present value of the three-year coupon bond in Years 1 and 2 (1 pt.). Note: The output of the expression or function you typed in this cell is expected as a positive number. Refer to the values from Steps 4 and 9 in your calculations. 11. In cell F17, by using cell references, calculate the implied price of the three-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 6 and 10 in your calculations. 12. In cell F18, by using cell references, calculate the yield to maturity of a three-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 4 and 11 in your calculations. 13. In cell G16, by using cell references and the function PV, calculate the present value of the four-year coupon bond in Years 1 thru 3 (1 pt.). Note: The output of the expression or function you typed in this cell is expected as a positive number. Refer to the values from Steps 4, 9, and 12 in your calculations. 14. In cell G17, by using cell references, calculate the implied price of the four-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 6 and 13 in your calculations. 15. In cell G18, by using cell references, calculate the yield to maturity of a four-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 4 and 14 in your calculations. Suppose you are given the information about the default-free, coupon-paying yield curve below. a. Use arbitrage to determine the yield to maturity of a two-year, zero-coupon bond. b. What is the zero-coupon yield curve for years 1 through 4? Par value of coupon bond $1,000 1 0.00% 2.000% $0.00 2 10.00% 3.908% 3 6.00% 5.840% 4 12.00% 5.783% Maturity (years) Coupon rate (annual payments) YTM Coupon amount Price of coupon bond Present value of interim coupon Implied price of zero-coupon bond Zero-coupon yield Requirements 1. Start Excel - completed. 2. In cell D18, by using a cell reference, input the zero-coupon yield for Year 1 (1 pt.). 3. In cell E14, by using cell references, calculate the coupon amount of the two-year coupon bond (1 pt.). 4. To calculate the coupon amounts of the three- and four-year coupon bonds, copy cell E14 and paste it onto cells F14:G14 (1 pt.). 5. In cell E15, by using cell references and the function PV, calculate the price of the two-year coupon bond (1 pt.). Note: The output of the expression or function you typed in this cell is expected as a positive number. 6. To calculate the price of the three- and four-year coupon bonds, copy cell E15 and paste it onto cells F15:G15 (1 pt.). 7. In cell E16, by using cell references and the function PV, calculate the present value of the two-year coupon bond in Year 1 (1 pt.). Note: The output of the expression or function you typed in this cell is expected as a positive number. 8. In cell E17, by using cell references, calculate the implied price of the two-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 5 and 7 in your calculations. 9. In cell E18, by using cell references, calculate the yield to maturity of a two-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 3 and 8 in your calculations. 10. In cell F16, by using cell references and the function PV, calculate the present value of the three-year coupon bond in Years 1 and 2 (1 pt.). Note: The output of the expression or function you typed in this cell is expected as a positive number. Refer to the values from Steps 4 and 9 in your calculations. 11. In cell F17, by using cell references, calculate the implied price of the three-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 6 and 10 in your calculations. 12. In cell F18, by using cell references, calculate the yield to maturity of a three-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 4 and 11 in your calculations. 13. In cell G16, by using cell references and the function PV, calculate the present value of the four-year coupon bond in Years 1 thru 3 (1 pt.). Note: The output of the expression or function you typed in this cell is expected as a positive number. Refer to the values from Steps 4, 9, and 12 in your calculations. 14. In cell G17, by using cell references, calculate the implied price of the four-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 6 and 13 in your calculations. 15. In cell G18, by using cell references, calculate the yield to maturity of a four-year zero-coupon bond (1 pt.). Note: Refer to the values from Steps 4 and 14 in your calculations

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts