Question: please show the excel reference Problem #2: Excel's Solver utility can also find an optimum solution involving more than one variable. We will use Solver

please show the excel reference

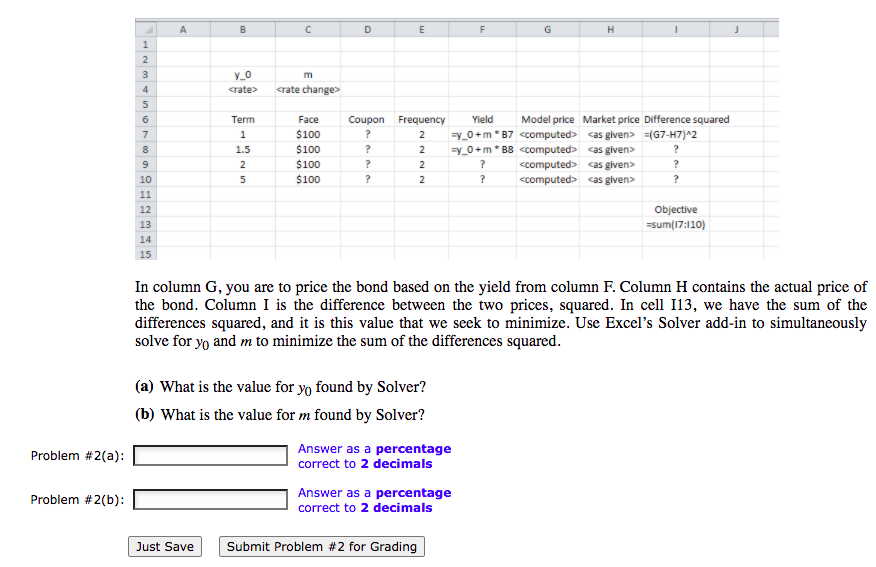

Problem #2: Excel's Solver utility can also find an optimum solution involving more than one variable. We will use Solver to find the best fit of a straight line yield curve for some bond prices (more information on Solver is available in the previous assignment, or in the online tutorial). You are to calibrate a straight line yield curve where y(t) = yo + mt by finding appropriate values for yo and m. The value y(t) is the semiannually compounding bond yield, or IRR, for a bond of maturity t. The yield curve is to be the best straight-line fit for the following four bonds: Bond 1 has face value $100 and a term of 1 year with semiannual coupons of 4% and a price of $98.00. Bond 2 has face value $100 and a term of 1.5 year with semiannual coupons of 6% and a price of $98.14. Bond 3 has face value $100 and a term of 2 year with a semiannual coupon of 7% and a price of $98.60. Bond 4 has face value $100 and a term of 5 year with a semiannual coupon of 5% and a price of $82.03. Create a spreadsheet with headings similar to the following: c A B D E F H 1 y_o m crate>

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts