Question: Please show Work and write neatly 8. Consider a trinomial tree for the Ho-Lee model where 0.02. The initial zero- coupon interest rate for maturities

Please show Work and write neatly

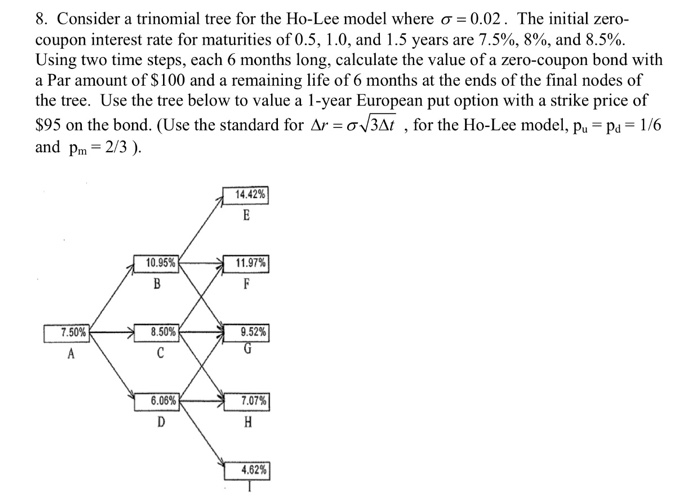

8. Consider a trinomial tree for the Ho-Lee model where 0.02. The initial zero- coupon interest rate for maturities of 0.5, 1.0, and 1.5 years are 7.5%, 8%, and 8.5%. Using two time steps, each 6 months long, calculate the value of a zero-coupon bond with a Par amount of $100 and a remaining life of 6 months at the ends of the final nodes of the tree. Use the tree below to value a 1-year European put option with a strike price of $95 on the bond. (Use the standard for Ar = 31 , for the Ho-Lee model, p,-p,-16 and pm 2/3). 14.42% 10.95%-- 11.97% 7.50% 8.50%-- 9.52% 6.06%- 7.07% 4.62%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock