Question: Please show work for each problem 1. The assets weights are 20%, 35% and 45% respectively, their standard deviations are 2.3%, 3.5% and 4%, the

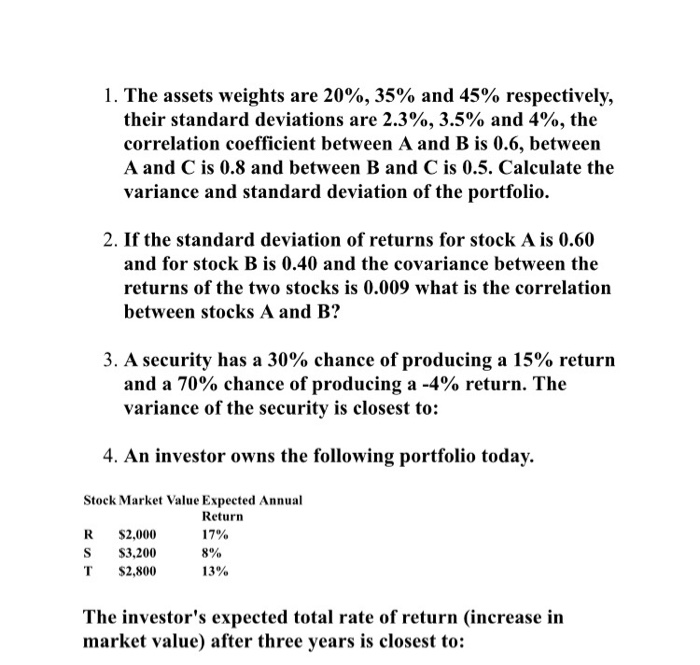

1. The assets weights are 20%, 35% and 45% respectively, their standard deviations are 2.3%, 3.5% and 4%, the correlation coefficient between A and B is 0.6, between A and C is 0.8 and between B and C is 0.5. Calculate the variance and standard deviation of the portfolio. 2. If the standard deviation of returns for stock A is 0.60 and for stock B is 0.40 and the covariance between the returns of the two stocks is 0.009 what is the correlation between stocks A and B? 3. A security has a 30% chance of producing a 15% return and a 70% chance of producing a -4% return. The variance of the security is closest to: 4. An investor owns the following portfolio today. Stock Market Value Expected Annual Return R $2,000 17% S $3,200 8% T $2,800 13% The investor's expected total rate of return (increase in market value) after three years is closest to

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts